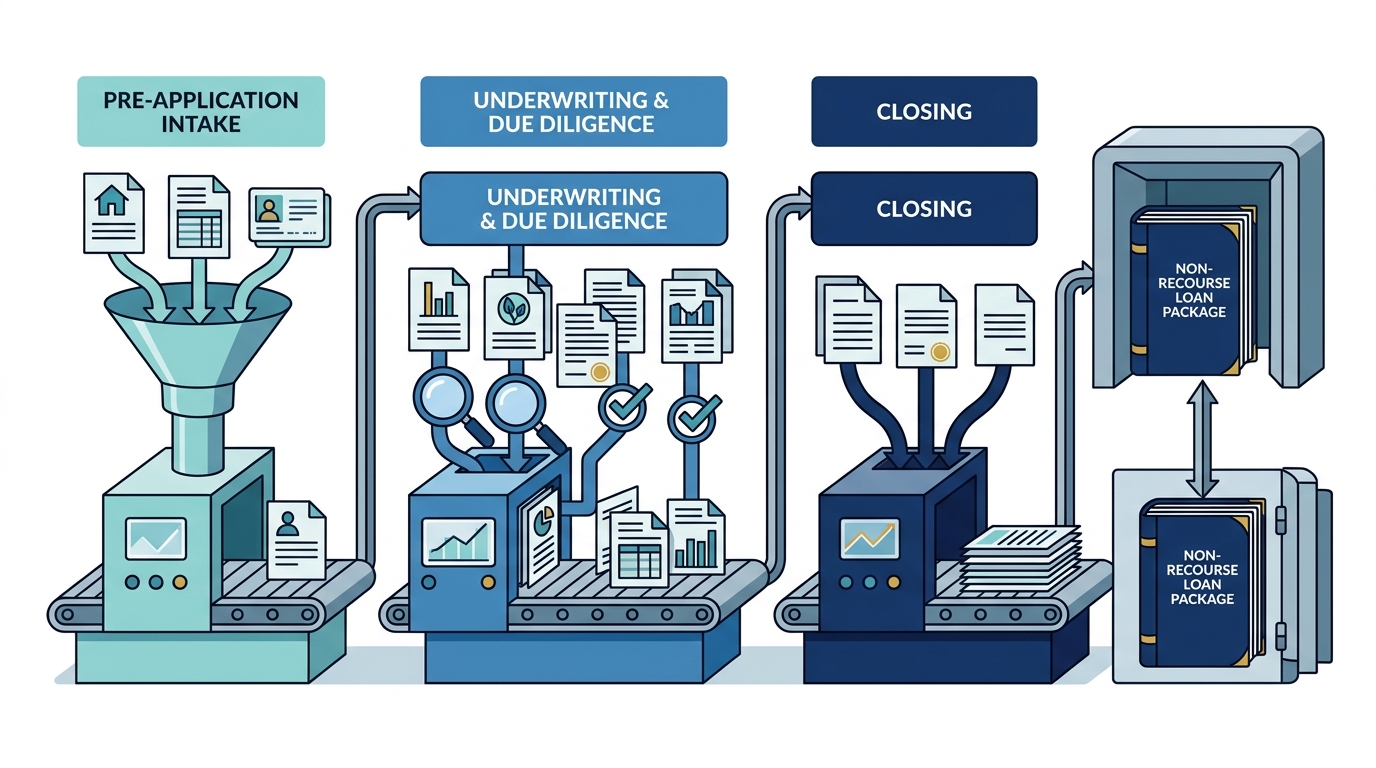

Non-recourse commercial real estate loans protect your personal assets from lender claims—but earning that protection means satisfying far more paperwork than a typical recourse deal. This tutorial walks you through every document you need, organized by the three stages lenders actually follow: pre-application intake, underwriting and due diligence, and closing.

Why Non-Recourse Documentation Is Different

In a standard recourse loan, the lender can pursue your personal bank accounts and primary residence if the property defaults. A non-recourse loan removes that safety net for the lender—the only recovery path is the collateral itself. Because lenders absorb more risk, they compensate with deeper scrutiny of the asset, the borrowing entity, and the sponsor's track record.

Non-recourse commercial loans are frequently made to special purpose entities (SPEs)—LLCs or similar vehicles created solely to own the collateral asset. This structure provides clean asset isolation and protects other business assets from claims related to the loan. SPE requirements alone introduce an entire layer of organizational documents that recourse borrowers never encounter.

Additionally, most non-recourse loans include "bad boy" carve-outs—provisions that can convert the loan to full recourse if the borrower commits fraud, misrepresents financials, or fails to maintain required insurance. Understanding these carve-outs is critical because the documents you sign will define exactly where your liability begins.

Phase 1 — Pre-Application Intake Documents

Before a lender issues a formal application or term sheet, they need enough information to determine whether your deal fits their program. Gathering these documents first prevents wasted time and deposit money.

1. Borrowing Entity Formation Papers

If the business is an LLC, provide Articles of Organization and the Operating Agreement. If it is a corporation, supply Articles of Incorporation and Bylaws. Most non-recourse lenders require a Single Purpose Entity (SPE) LLC to limit exposure, so have your SPE formation documents ready—including any amendments that reflect bankruptcy-remote provisions such as an independent director requirement.

2. Organizational Chart

An organizational chart visually depicts how the borrowing entity is structured. In commercial real estate, organizational structures can be complex, particularly if joint ventures, trusts, or mezzanine debt are involved. Lenders use the org chart to identify every party with an ownership stake and confirm the SPE is properly isolated.

3. Personal Financial Statement (PFS)

Even though personal guarantees are not required, the borrowing entity's sponsor still undergoes financial vetting. A PFS—typically on ABA or SBA Form 413—lists the sponsor's assets, liabilities, and net worth. Many lenders require the PFS to be dated within the past 60 days. Non-recourse commercial mortgage loans are generally only available to borrowers who are very strong financially.

4. Schedule of Real Estate Owned (SREO)

An SREO lists all other real estate investments the sponsor owns, including estimated value, current NOI, and outstanding loan balances. This document proves the sponsor's track record and demonstrates experience managing comparable properties—a threshold requirement for non-recourse financing.

5. Sponsor Résumés

Commercial mortgage lenders require a very experienced borrower for a non-recourse loan. Provide résumés for each key principal, emphasizing relevant asset-class experience, portfolio size, and years active in commercial real estate.

6. Property Summary & Photos

A brief narrative describing the property type, location, unit count or square footage, year built, recent renovations, and current occupancy—accompanied by interior and exterior photographs—gives the lender a quick snapshot before deeper analysis begins.

Phase 2 — Underwriting & Due-Diligence Documents

Once the lender issues an application or term sheet (and you pay the good-faith deposit, which can be $35,000 or more on CMBS deals), the underwriting engine engages. This phase typically spans 30 to 90 days and is the most document-intensive stage.

7. Three Years of Historical Operating Statements

Provide year-end property income and expense statements for the most recent three years, ideally in spreadsheet format. The lender's analyst will normalize these figures—stripping out one-time expenses and capital items—to arrive at stabilized net operating income (NOI).

8. Trailing-12-Month Income & Expense Report

Beyond historical annual statements, most lenders want a month-by-month income and expense breakdown for the most recent 12 months. This granular view reveals seasonal patterns, vacancy trends, and expense spikes the annual totals might mask.

9. Current Rent Roll

A rent roll lists every tenant currently paying rent on the property, including lease start and end dates, which tenants are behind on their rent, and any rental concessions provided. It is one of the most effective tools lenders use to calculate collateral risk.

10. Lease Expiration Schedule & Copies of Major Leases

A lease expiration schedule shows when each lease expires and what percentage of total leasable area each lease represents. For office, retail, and industrial assets, lenders will also request copies of all tenant leases—or at minimum, leases representing the largest revenue concentrations.

11. Borrower and Sponsor Tax Returns

Provide the three most recent years of tax returns for both the borrowing entity and each key principal. If the borrower is a disregarded entity that does not file separate returns, be prepared to negotiate an appropriate exception with the lender's counsel.

12. Third-Party Appraisal

An MAI-certified appraisal is ordered (and paid for by the borrower) to confirm the property's market value. The resulting loan-to-value ratio is a critical gatekeeping metric; in 2026, most non-recourse programs require an LTV between 65% and 75%.

13. Phase I Environmental Site Assessment

A Phase I ESA checks for soil or water contamination. If the Phase I flags potential issues, a Phase II with soil sampling follows. Environmental liability is a major concern because the property is the lender's sole recourse in a default.

14. Property Condition Report (PCR)

An engineer inspects the structural, mechanical, electrical, plumbing, and roofing systems. The PCR quantifies deferred maintenance and recommends an escrow reserve for immediate and long-term repairs—funds the lender will likely require you to set aside at closing.

15. Seismic Risk Assessment (If Applicable)

Properties in seismic zones (California, Pacific Northwest, parts of the Midwest) may require a Probable Maximum Loss (PML) report. If the PML exceeds a threshold—typically 20%—the lender will require earthquake insurance.

16. Zoning Compliance Letter or Report

A zoning report confirms the property's current use is legally permitted and identifies any non-conforming conditions. CMBS lenders are especially rigorous here because post-securitization, no one at the servicer level will negotiate a zoning variance on your behalf.

17. Survey

An ALTA/NSPS survey identifies boundaries, easements, encroachments, and flood-zone designations. The title company and lender both rely on this document to confirm the legal description matches what is being financed.

18. Title Commitment & Title Insurance

A preliminary title commitment reveals liens, encumbrances, and exceptions. The lender will require a lender's title insurance policy at closing to protect against title defects discovered after funding.

Phase 3 — Closing & Post-Closing Documents

At this stage, the lender's counsel drafts (or finalizes) the formal loan documents. For CMBS transactions, many provisions are non-negotiable because they are structured to protect bond investors who will eventually hold the loan.

19. Promissory Note

The note sets forth the loan amount, interest rate, amortization schedule, maturity date, and prepayment provisions (yield maintenance or defeasance). Review the default interest rate and late-charge provisions carefully.

20. Mortgage or Deed of Trust

This is the recorded instrument that gives the lender a lien on the property. It references the note and contains covenants about property maintenance, insurance, and permitted transfers.

21. Assignment of Leases and Rents

The borrower assigns its interest in all current and future leases as additional security. In a default scenario, this document lets the lender step into the borrower's shoes to collect rent directly from tenants.

22. Environmental Indemnity Agreement

Even in a non-recourse structure, environmental indemnity is almost always a personal obligation of the sponsor. This carve-out means contamination-related losses can follow you personally, making the Phase I ESA results especially important.

23. Non-Recourse Carve-Out Guaranty

A designated guarantor (often the sponsor or a principal) signs a guaranty covering the "bad boy" carve-outs. Typical triggers include fraud, misrepresentation, voluntary bankruptcy filing, misappropriation of rents or insurance proceeds, and failure to maintain required insurance. This guaranty is arguably the most consequential document in the entire package because it defines the boundary between limited and full recourse.

24. SPE & Bankruptcy-Remote Compliance Certificate

The borrower certifies compliance with all SPE covenants—including that an independent director or manager is in place and that no assets other than the subject property are held in the entity. Violations of SPE covenants typically trigger recourse liability under standard CMBS loan documents.

25. Borrower Counsel Opinion Letters

The borrower's attorney delivers legal opinions on entity authority, enforceability of the loan documents, and sometimes a "true lease" or non-consolidation opinion. Hire an attorney experienced in CMBS closings—inexperienced counsel can add thousands in extra legal fees by attempting to negotiate non-negotiable provisions.

26. Insurance Certificates

Before funding, you must deliver evidence of all required insurance: hazard/property coverage, general liability, loss of rents/business interruption, and (where applicable) flood, earthquake, and terrorism coverage. The lender is named as mortgagee and loss payee.

27. Cash Management & Lockbox Agreements

Almost every non-recourse (and especially CMBS) loan requires a cash management structure. Tenants may be directed to remit rent to a lender-controlled lockbox account, from which operating expenses and debt service are disbursed according to a waterfall defined in the loan agreement.

How Document Requirements Shift by Lender Type

| Lender Type | Typical Deal Size | Unique Documentation Demands |

|---|---|---|

| CMBS Conduit | $2M–$100M+ | SPE with independent director; defeasance provisions; rating-agency confirmation language; lockbox from day one |

| Life Insurance Company | $5M–$500M+ | Detailed environmental due diligence; conservative underwriting with audited financials preferred; longer approval timeline |

| Agency (Fannie Mae / Freddie Mac) | $1M–$100M+ (multifamily) | Replacement-reserve escrow; property management approval; green-certification documentation if pursuing sustainability incentives |

| Private / Hard Money (Non-Recourse) | $500K–$20M | Shorter document list but higher equity required; exit-strategy documentation (sale comps or refi term sheet); guaranteed maximum price contracts for construction |

Regardless of lender type, the core documentation categories—entity formation, financials, third-party reports, and closing instruments—remain consistent. The depth and formality increase as you move from private lenders toward institutional capital.

Common Mistakes That Delay Non-Recourse Deals

- Submitting a stale PFS. If your personal financial statement is older than 60 days, most lenders will reject it and the clock restarts.

- Using a general-purpose LLC. Non-recourse lenders need a dedicated SPE. Trying to retrofit an existing entity with bankruptcy-remote language mid-process causes legal delays.

- Incomplete rent rolls. Missing lease terms, tenant contact info, or concession details force the underwriter to send follow-up requests, adding weeks.

- Ignoring the environmental indemnity. Borrowers often focus on the non-recourse label without realizing the environmental carve-out creates personal exposure. Review the Phase I before signing.

- Hiring inexperienced legal counsel. CMBS loan documents are extensive and many provisions cannot be changed. An attorney unfamiliar with securitized lending may waste time and money negotiating non-negotiable points.

Key Takeaways

- Non-recourse loans demand more documentation, not less. The lender's inability to pursue personal assets makes property-level and entity-level paperwork far more rigorous than a recourse loan.

- Form your SPE early. A Single Purpose Entity with bankruptcy-remote provisions is a baseline requirement for virtually every non-recourse commercial lender.

- Prepare financials before you shop. Three years of operating statements, a current rent roll, a fresh PFS, and an SREO should be ready the day you contact a lender.

- Budget for third-party reports. Appraisal, Phase I ESA, property condition report, survey, and zoning report costs are borrower-paid and can total $30,000–$75,000 on larger deals.

- Read every carve-out. The non-recourse carve-out guaranty defines where limited liability ends and full personal recourse begins—it is the single most important document to scrutinize.

Frequently Asked Questions

What is a non-recourse commercial real estate loan?

A non-recourse loan is a secured loan that limits the lender, in the event of default, to proceed only against the collateral—the commercial property itself. The lender cannot pursue the borrower's personal assets, bank accounts, or other properties to recover losses.

Do non-recourse loans still require a personal guarantee?

Not a full personal guarantee, but they do require a non-recourse carve-out guaranty. This makes the sponsor personally liable for specific "bad boy" acts like fraud, voluntary bankruptcy, or misappropriation of rents and insurance proceeds.

What minimum DSCR do lenders require for non-recourse financing?

Most non-recourse commercial real estate loans require a debt service coverage ratio (DSCR) of 1.25x or higher, meaning the property generates at least 25% more net operating income than the annual debt service.

How long does it take to close a non-recourse commercial loan?

Non-recourse commercial loans typically take 45 to 90 days to close, compared to 30 to 60 days for conventional recourse loans. CMBS loans specifically often take 60 to 90 days due to securitization-related requirements.

What LTV can I expect on a non-recourse deal?

Most non-recourse lenders cap LTV between 65% and 75%, meaning you need 25% to 35% equity in the property. Lower LTV reduces the lender's exposure and is a core trade-off for eliminating personal recourse.

Can I use Lendersa to compare non-recourse loan options?

Yes. Lendersa is a loan marketplace that connects borrowers with competing lenders—including both conventional and hard money programs—for residential, commercial, and vacant land properties. You can compare non-recourse offers side by side, and AI matching helps surface lenders whose programs fit your deal profile. No SSN is required to start.