Private real estate lending has expanded rapidly, with industry reports indicating that non-bank mortgage originations now exceed forty percent of all residential funding. This shift creates significant opportunities for investors, but it also introduces complex verification challenges. Borrowers must distinguish between regulated capital providers and predatory operators before committing to any agreement. Understanding the exact mechanics of private financing protects your equity and prevents irreversible financial damage. You can evaluate any financing offer by examining licensing, fee transparency, and default protocols. According to the Federal Trade Commission, non-bank lending now represents a dominant market segment.

Understanding Private Lending Structures

A private lender is a non-institutional financial entity that provides capital based on asset value rather than traditional credit scores. These entities typically fund fix and flip projects, construction ventures, or bridge financing scenarios. Legitimate operators follow standardized underwriting guidelines and maintain transparent communication channels throughout the funding lifecycle. You should always verify that the capital source maintains proper escrow arrangements and adheres to state-specific usury laws. When you review the borrower portal, you gain immediate access to standardized program comparisons that filter out unverified operators.

Core Funding Models Explained

Most legitimate private lenders structure their capital around loan-to-value ratios ranging from sixty-five to eighty percent. This conservative approach ensures that the underlying property maintains sufficient equity to cover the principal balance. Predatory operators frequently bypass these safeguards by offering one hundred percent financing without proper collateral verification. You must demand a clear amortization schedule and verify that all points are disclosed before signing any commitment letter.

Red Flags in Loan Documentation and Fees

Transparent fee structures remain the primary differentiator between regulated capital providers and predatory operators. Legitimate lenders itemize origination fees, processing charges, and underwriting costs within the initial Good Faith Estimate. You will notice immediate warning signs when an operator demands upfront payments before completing a title search or property appraisal. These advance fees often vanish without triggering any actual funding process. Always request a detailed breakdown of all closing costs before transferring any initial deposits.

Hidden Cost Indicators

Excessive prepayment penalties represent another common predatory tactic. Legitimate hard money loans typically allow early repayment without triggering double-digit penalty fees. You should carefully review the promissory note for clauses that restrict refinancing or impose arbitrary default triggers. If the documentation lacks clear default definitions, you should pause the transaction and consult a qualified real estate attorney. The frequently asked questions section on our platform outlines standard contractual protections that every borrower should request.

Verifying Licensing and Regulatory Compliance

Regulatory compliance serves as the foundational filter for identifying legitimate private lenders. Every legitimate capital provider must maintain active registration with state financial regulatory agencies and national licensing databases. You can verify any operator by cross-referencing their business entity against the Nationwide Multistate Licensing System. Legitimate lenders also publish clear privacy policies and maintain physical business addresses that match their operational headquarters. When you explore the founder background, you will see how decades of regulatory adherence build sustainable lending ecosystems.

Compliance Verification Steps

Always request proof of insurance, surety bonds, and fiduciary responsibility documentation before advancing your application. Legitimate operators maintain these requirements to protect both the borrower and the underlying collateral. You should never accept verbal assurances regarding compliance status. Written documentation must explicitly state the lender's registration number and jurisdictional authority. This verification process eliminates unregistered entities that operate outside standard financial oversight frameworks.

Assessing Repayment Terms and Default Consequences

Default consequences define the actual risk exposure for every real estate investor. Legitimate private lenders structure foreclosure protocols according to state judicial or non-judicial timelines. You will encounter predatory operators when they demand immediate full repayment upon minor payment delays or impose arbitrary acceleration clauses. Standard industry practice allows a thirty-day cure period before initiating formal default proceedings. Always review the conventional and private loan routing guidelines to understand how legitimate operators handle payment discrepancies.

Interest Rate and Amortization Standards

Private lending rates typically range from eight to fifteen percent depending on the asset class and risk profile. Legitimate lenders calculate interest using standard daily interest accrual methods rather than flat-fee structures. You should verify that the interest calculation aligns with the actual disbursement date and closing timeline. Predatory operators frequently manipulate interest calculations to inflate the total repayment amount beyond reasonable market benchmarks. Clear amortization schedules prevent unexpected balance shocks during the funding period.

Utilizing AI Matching Platforms for Verification

Advanced matching technology has revolutionized how borrowers evaluate private lending options. Modern platforms utilize proprietary algorithms to cross-reference thousands of capital programs against specific property parameters. You can instantly compare hard money offers or bank loans without submitting sensitive identification documents. This automated verification process filters out unverified operators and highlights programs that match your exact risk profile. The capital portal demonstrates how structured matching protocols eliminate manual verification errors.

Automated Risk Assessment Benefits

AI-driven matching systems evaluate loan-to-value ratios, debt-service coverage ratios, and geographic market trends simultaneously. You receive standardized program comparisons that highlight legitimate operators based on historical performance metrics. This automated filtering process removes subjective bias and ensures that every recommended lender meets baseline compliance standards. Borrowers who utilize these platforms consistently secure faster closings with reduced documentation requirements. The Lendersa platform provides a secure environment for comparing these verified programs.

Key Takeaways

- Private real estate lending now accounts for over forty percent of non-bank residential funding.

- Legitimate operators maintain active state registrations and publish transparent fee schedules.

- Upfront advance fees before title verification represent a primary predatory indicator.

- Standard loan-to-value ratios typically range from sixty-five to eighty percent.

- AI matching platforms filter thousands of programs to highlight verified capital providers.

- Thirty-day cure periods remain standard industry practice before default initiation.

- Proprietary tools like LoanScore™ and LoanImprove™ streamline the verification process.

Frequently Asked Questions

How do I verify a private lender's state registration?

You can verify any private lender by searching their business entity name in your state's financial regulatory database. Legitimate operators must maintain active registration numbers and publish their physical business addresses. You should cross-reference these details against the Nationwide Multistate Licensing System to confirm operational authority.

What constitutes a legitimate loan-to-value ratio?

A legitimate loan-to-value ratio typically ranges from sixty-five to eighty percent for most private real estate transactions. This conservative threshold ensures that the underlying property maintains sufficient equity to cover the principal balance. You should request a formal appraisal before accepting any financing offer that exceeds these standard parameters.

Are upfront fees legal in private lending?

Upfront processing fees remain legal when clearly disclosed in the initial Good Faith Estimate. You should never pay advance funding fees before completing a title search or property appraisal. Legitimate operators structure these costs to close alongside standard settlement expenses.

How quickly can legitimate private lenders fund a transaction?

Legitimate private lenders typically fund transactions within seven to fourteen business days. This timeline allows sufficient time for title verification, environmental assessments, and regulatory compliance checks. You should expect faster closings only when all documentation is pre-approved and the property meets standard underwriting criteria.

What happens if I miss a single payment on a private loan?

Standard industry practice allows a thirty-day cure period before initiating formal default proceedings. Legitimate lenders will notify you in writing and provide clear instructions for resolving the payment discrepancy. You should review your promissory note for specific grace period clauses before assuming immediate foreclosure triggers.

Can I refinance a private loan before the original term expires?

Most legitimate private lenders allow early repayment without triggering excessive penalty fees. You should verify the prepayment clause in your commitment letter before signing any agreement. Predatory operators frequently impose double-digit penalties to restrict refinancing options and lock borrowers into unfavorable terms.

How does AI matching improve lender verification?

AI matching systems evaluate thousands of capital programs against specific property parameters simultaneously. You receive standardized program comparisons that highlight legitimate operators based on historical performance metrics. This automated filtering process removes subjective bias and ensures that every recommended lender meets baseline compliance standards.

Next Steps for Secure Financing

Securing legitimate private capital requires systematic verification and structured comparison. You should utilize automated matching platforms to filter thousands of programs against your exact property parameters. This approach eliminates manual verification errors and highlights operators that meet baseline compliance standards. Visit the Lendersa homepage to explore our proprietary matching tools and begin comparing verified programs today.

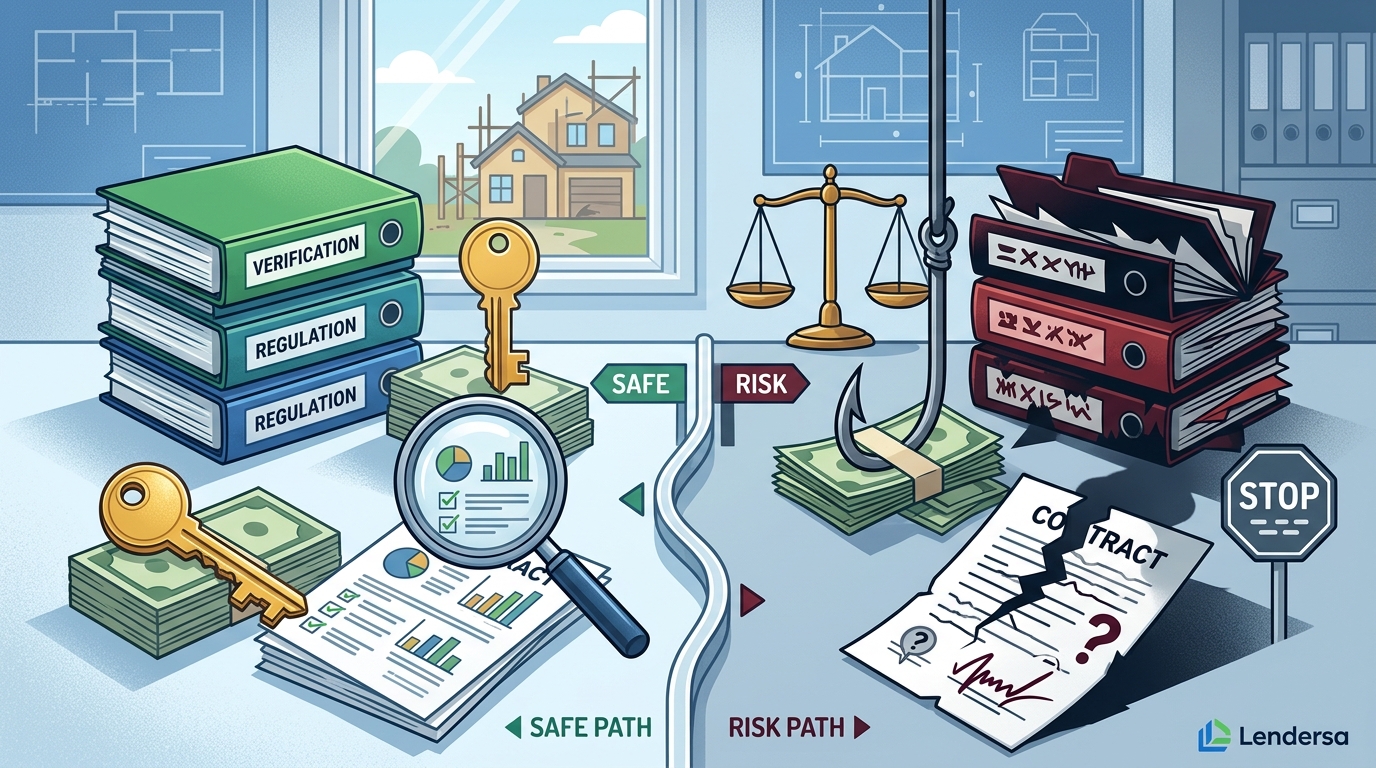

| Verification Metric | Legitimate Private Lender | Predatory Operator |

|---|---|---|

| State Registration Status | Active and verifiable | Unregistered or missing |

| Fee Disclosure Structure | Itemized in Good Faith Estimate | Hidden or vague clauses |

| Loan-to-Value Ratio | 65% to 80% standard | Exceeds 90% without collateral |

| Default Cure Period | 30-day written notice | Immediate acceleration |

| Technology Integration | AI-matched programs | Manual paper processing |