Securing capital for undeveloped parcels or distressed residential properties requires specialized financing channels. According to the Federal Reserve, nontraditional mortgage lending grew by nearly 40 percent between 2020 and 2023, driven by borrowers who fall outside conventional underwriting guidelines. Nontraditional lending fills this gap by prioritizing asset value over credit scores. Lendersa® leverages advanced AI to match your specific scenario with hundreds of direct hard money lenders, private money lenders, and banks. You can view hard money offers or bank loans instantly without submitting a Social Security Number. This streamlined approach removes traditional friction and accelerates your path to closing.

Understanding Vacant Land Financing

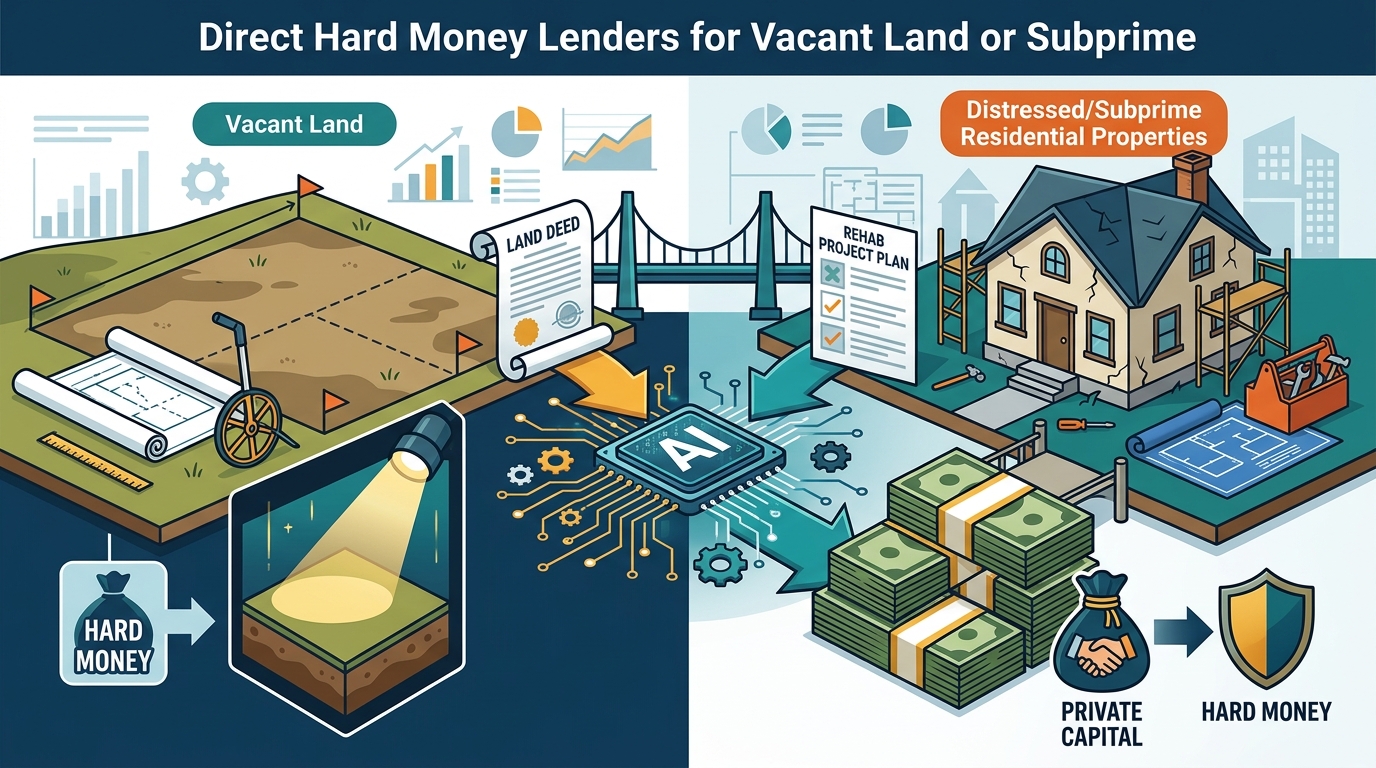

Hard money lenders specialize in short-term, asset-based capital. A hard money loan is a short-term, asset-based financing instrument secured by real estate collateral rather than borrower creditworthiness. Lenders evaluate the after-repair value or current land value to determine loan-to-value ratios. Vacant land financing often carries higher interest rates because undeveloped parcels lack immediate cash flow. Direct hard money lenders bypass traditional bank bureaucracy to fund these transactions quickly. You can explore state-specific fix and flip lenders by visiting our Fix and Flip Lenders by State directory. This resource filters programs by geographic jurisdiction and capital availability.

Raw land transactions require precise valuation models. Lenders assess zoning classifications, environmental reports, and access infrastructure before approving capital. Many direct hard money lenders for vacant land or subprime residential loans structure deals around clear exit strategies. You must demonstrate a viable development plan or resale timeline to secure favorable terms. Our platform evaluates your project parameters and routes them to compatible capital sources automatically.

Navigating Subprime Residential Loans

Subprime residential loans target borrowers with damaged credit histories or non-traditional income streams. A subprime residential loan is a mortgage product designed for borrowers with credit scores below 620 or complex financial profiles. Traditional banks often reject these applications due to rigid risk models. Direct hard money lenders focus on the property's equity and rehabilitation potential instead. Our Borrowers portal allows you to submit your scenario without triggering a hard credit pull. The system evaluates your project parameters and routes them to compatible capital sources.

Distressed properties frequently require substantial renovation capital. Lenders calculate the after-repair value to determine maximum funding limits. Subprime borrowers benefit from flexible debt-to-income calculations when sufficient equity exists. Our Conventional and Private Loan Routing framework ensures your project reaches lenders actively seeking your asset class. This method preserves your credit score while securing competitive terms. You can review our Frequently Asked Questions section to understand the exact documentation requirements for each category.

How AI Matches Direct Lenders

Manual broker searches waste weeks on unresponsive lenders and outdated programs. Lendersa® uses advanced AI to instantly match your loan scenario with hundreds of hard money lenders, private money lenders, and banks. The platform runs a Multi-Lender Protocol that evaluates your project against active capital pools. Only the top matching programs are compared automatically. Whether you are looking for the lowest rates on conventional mortgages or fast closings from top-tier hard money lenders, our system balances speed and cost.

A Multi-Lender Protocol is an automated routing system that matches borrower scenarios against active capital pools to optimize terms and speed. The engine filters thousands of lender programs to surface the exact capital source your project requires. You can submit multiple project parameters and receive customized routing for each asset. Our proprietary AI tools evaluate interest rates, points, prepayment penalties, and draw schedules simultaneously. This computational approach eliminates human bias and accelerates decision-making. You can review our About Lendersa page to learn how our founding team revolutionized real estate finance.

Comparing Lending Structures

Different loan structures serve distinct investment strategies. The table below outlines the primary financing options available through our network.

| Loan Type | Typical Loan-to-Value Ratio | Best Use Case | Processing Timeline |

|---|---|---|---|

| Vacant Land Loan | 50 to 65 percent | Raw land acquisition or zoning changes | 7 to 14 days |

| Fix and Flip Loan | 65 to 75 percent | Renovation projects and rapid resale | 5 to 10 days |

| Subprime Residential Loan | 70 to 80 percent | Distressed properties with weak credit | 10 to 21 days |

| Construction Loan | 75 to 85 percent | New builds or major structural upgrades | 14 to 30 days |

Each structure carries distinct risk parameters and repayment schedules. Direct hard money lenders adjust their terms based on your exit strategy and equity position. Our platform calculates the total cost of capital rather than focusing solely on monthly payments. You can compare hard money offers or bank loans instantly without paying pre-application fees. This transparency allows investors to model cash flows accurately before committing to a contract.

Key Takeaways

- Direct hard money lenders prioritize collateral value over personal credit scores.

- Vacant land financing typically requires 50 to 65 percent loan-to-value ratios.

- Subprime residential loans accommodate credit scores below 620 when equity exists.

- Lendersa® processes thousands of lender programs using proprietary AI matching.

- The Multi-Lender Protocol routes your project to active capital pools instantly.

- No Social Security Number is required to view initial hard money offers.

- Founding team brings over 35 years of direct lending experience to the platform.

Frequently Asked Questions

Can I secure direct hard money lenders for raw land without a credit check?

Yes. Direct hard money lenders evaluate the land value and your equity contribution. Our Borrowers portal allows you to view offers without triggering a hard credit inquiry.

What defines a subprime residential loan in the current market?

A subprime residential loan is a mortgage product designed for borrowers with credit scores below 620 or complex financial profiles. Lenders focus on property equity rather than traditional debt-to-income ratios.

How long does it take to close a vacant land hard money loan?

Closing timelines typically range from 7 to 14 days. Direct hard money lenders streamline documentation to accelerate funding for time-sensitive acquisitions.

Does Lendersa charge upfront fees to browse lender programs?

No. Our platform operates on a transparent matching model. You can compare hard money offers or bank loans instantly without paying pre-application fees.

What is the maximum loan-to-value ratio for subprime residential loans?

Most direct hard money lenders cap subprime residential loans at 70 to 80 percent loan-to-value. Higher equity contributions reduce interest rates and monthly payments.

Can I use AI to find direct hard money lenders for multiple properties?

Absolutely. Our Multi-Lender Protocol scales to handle portfolio acquisitions. You can submit multiple project parameters and receive customized routing for each asset.

Start Your Capital Search Today

Finding the right financing channel determines your project's profitability. Direct hard money lenders for vacant land or subprime residential loans operate outside traditional banking constraints. Our AI engine filters thousands of programs to surface the exact capital source your project requires. Begin your search today by visiting https://www.lendersa.com to connect with active lenders.