Private lending has expanded rapidly, with recent market data showing that over 40 percent of fix and flip transactions now rely on non-bank capital. This shift creates significant exposure to unvetted operators who prioritize speed over compliance. Borrowers must distinguish between regulated financing partners and predatory operators before signing any agreement. Understanding the exact mechanics of bridge financing protects your equity and prevents catastrophic debt traps. Industry reports indicate that fraudulent lending schemes cost investors nearly 2.3 billion dollars annually across residential markets. (Get Answers For Hard)

Understanding Private Lending Fundamentals

Private lending is capital provided by non-institutional investors or specialized firms rather than traditional banks. These entities evaluate properties based on asset value instead of personal credit scores. This approach accelerates approval timelines and expands access to complex transactions. Hard money loan is a short-term asset-based financing product secured exclusively by real estate collateral. Investors utilize these instruments to acquire distressed properties, execute renovations, and refinance into conventional mortgages. Legitimate operators maintain transparent underwriting guidelines and publish clear amortization schedules. Predatory actors obscure these details to extract maximum value from desperate borrowers. (Compare Hard Money amp)

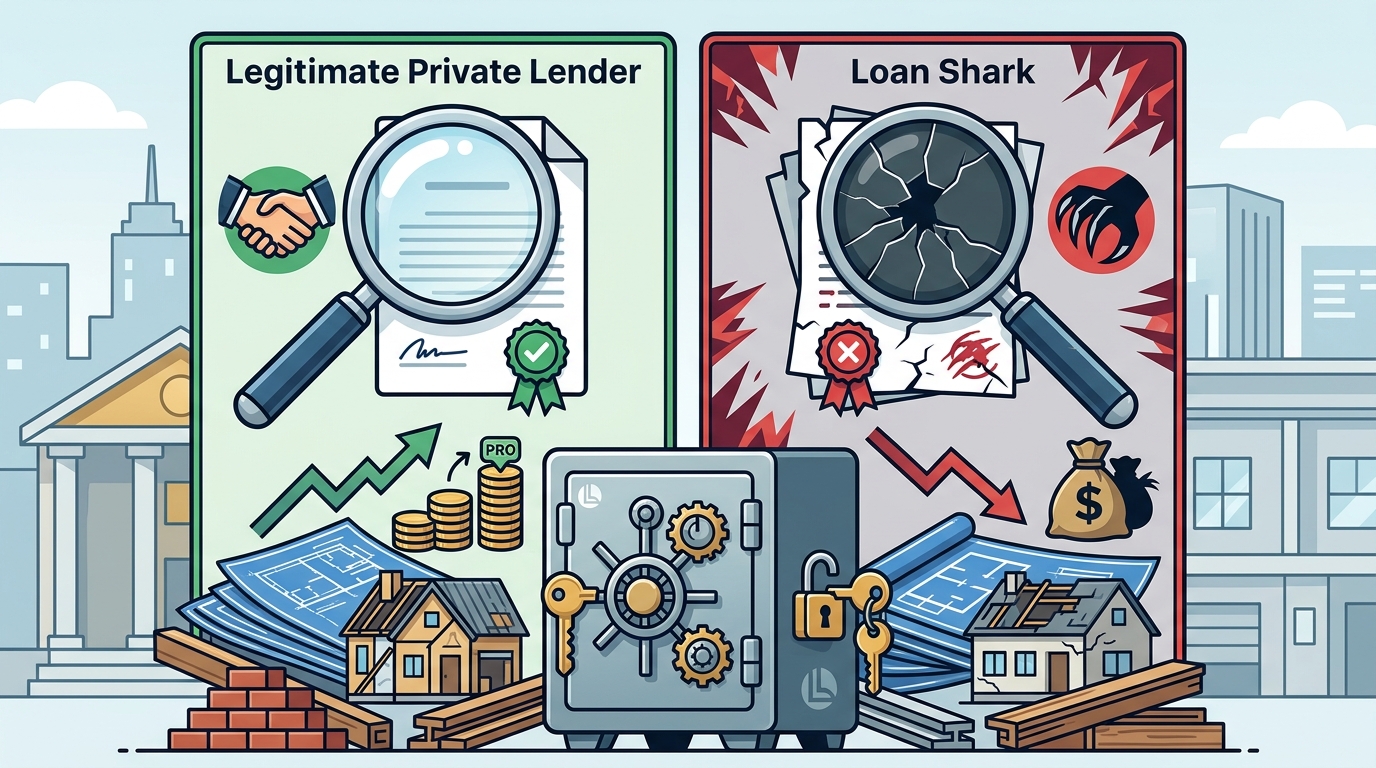

Red Flags That Signal Predatory Practices

Loan shark is an unlicensed operator who charges exorbitant interest rates and enforces aggressive collection tactics. You can spot these entities by examining their communication patterns and document requests. Legitimate lenders request standard property appraisals, title reports, and renovation budgets. Predatory operators demand upfront fees before reviewing any documentation. They also pressure borrowers to sign blank promissory notes or waive standard disclosure rights. Always verify that all fees are disclosed in writing before transferring any funds. Regulatory agencies track these warning signs to issue consumer alerts and enforce penalties. You should request a complete fee schedule and compare it against state usury limits. Discrepancies between verbal promises and written contracts indicate immediate termination of negotiations.

Verifying Licensing and Regulatory Compliance

Every legitimate financing partner must operate under state-specific lending licenses. You can verify these credentials through official state banking department portals. Unlicensed operators frequently operate across jurisdictional boundaries to avoid regulatory oversight. The Federal Trade Commission tracks these violations and publishes enforcement actions annually. You should cross-reference the lender name with your state's official registry. Legitimate platforms also maintain clear physical addresses and verifiable corporate registration numbers. Predatory entities often use shell companies or frequently change business names to evade accountability. Always request a copy of the lender's current license before signing any agreement. Compliance checks also reveal whether the operator adheres to fair lending practices and anti-discrimination statutes. You can access detailed compliance records through official government databases.

Analyzing Fee Structures and Repayment Terms

Transparent pricing models separate professional operators from predatory lenders. Legitimate lenders disclose origination fees, underwriting costs, and prepayment penalties in advance. Predatory operators hide these costs inside inflated interest rates or hidden administrative charges. Recent market analysis shows that average hard money rates range between 8 percent and 15 percent annually. You should calculate the total cost of capital using a standardized amortization calculator. Hidden clauses often include balloon payments, compound interest triggers, or unilateral modification rights. Always review the complete repayment schedule before committing to any financing package. Professional lenders also offer flexible exit strategies and clear default remedies. Predatory entities enforce harsh foreclosure procedures and charge excessive late payment penalties. You can compare these structures using standardized financial modeling tools.

Leveraging AI Matching to Filter Risk

Modern lending platforms utilize automated matching protocols to screen thousands of programs instantly. These systems evaluate borrower scenarios against verified lender criteria without requiring sensitive personal data. You can access these tools through official platform portals to compare multiple offers simultaneously. The Multi-Lender Protocol evaluates speed, cost, and compliance metrics to surface the optimal financing path. Always utilize automated comparison tools to eliminate manual research errors. These platforms also flag non-compliant programs and restrict access to unverified operators. You can explore these resources through the official borrower dashboard to streamline your search. The system balances speed and cost to find the absolute best program for your property. You can review detailed program comparisons through the official capital portal interface.

| Financing Option | Verification Requirement | Typical Use Case | Platform Integration |

|---|---|---|---|

| Fix and Flip Loans | Asset-based appraisal | Renovation projects | Borrower Dashboard |

| Construction Financing | Phase-based disbursements | New builds | Private Loan Routing |

| Bridge Financing | Exit strategy validation | Temporary holds | Program FAQ |

| Commercial Capital | Debt service coverage | Multi-unit assets | Capital Portal |

Key Takeaways

- Private lending accounts for over 40 percent of fix and flip transactions in current markets.

- Fraudulent lending schemes cost investors nearly 2.3 billion dollars annually across residential markets.

- Legitimate operators require standard appraisals, title reports, and renovation budgets before approval.

- Predatory entities demand upfront fees before reviewing any documentation or property details.

- State banking departments maintain official registries to verify current lending licenses.

- Automated matching protocols screen thousands of programs without requiring sensitive personal data.

- Professional platforms maintain clear physical addresses and verifiable corporate registration numbers.

Frequently Asked Questions

How do I verify if a private lender holds a valid state license?

You can verify credentials through official state banking department portals. These registries list active licenses, expiration dates, and disciplinary actions. You should cross-reference the lender name with your state's official database before signing any agreement.

What is the maximum interest rate allowed for private loans?

State usury laws dictate maximum allowable rates for private financing. These limits vary significantly across jurisdictions and transaction types. You should consult official regulatory guidelines to determine the exact threshold for your specific location.

Can legitimate lenders require upfront fees before approval?

Legitimate lenders rarely require substantial upfront payments before underwriting. They typically charge minimal application fees to cover administrative costs. You should request a complete fee schedule and compare it against state regulations.

How does automated matching technology improve lender verification?

Automated matching technology screens thousands of programs instantly. These systems evaluate borrower scenarios against verified lender criteria. You can access these tools through official platform portals to compare multiple offers simultaneously.

What documents do professional lenders require for approval?

Professional lenders request standard property appraisals, title reports, and renovation budgets. They also require proof of funds and clear exit strategies. You should prepare these documents to streamline the approval process.

How can I identify hidden penalties in private loan agreements?

You should calculate the total cost of capital using a standardized amortization calculator. Hidden clauses often include balloon payments, compound interest triggers, or unilateral modification rights. Always review the complete repayment schedule before committing to any financing package.

What steps should I take if I suspect predatory lending practices?

You should document all communications and preserve every written agreement. You can report suspicious activity to state banking regulators and federal consumer protection agencies. You should also consult legal counsel to review your contractual obligations.

Secure Your Financing Today

Identifying legitimate private lenders requires systematic verification, transparent documentation, and automated screening tools. You can streamline this process by utilizing advanced matching protocols that evaluate hundreds of programs instantly. Start your financing search today to compare verified offers without sharing sensitive personal data. Our platform balances speed and cost to find the absolute best program for your property. Visit the official borrower dashboard to explore available programs and secure your next investment.