The landscape of commercial and residential lending has shifted dramatically from manual outreach to algorithmic precision. According to recent industry analyses, borrowers who utilize automated comparison tools secure financing up to 40% faster than those relying on traditional broker networks. This acceleration is not merely a matter of convenience but a structural necessity in a market where capital velocity dictates deal success. Lenders and borrowers alike must adapt to a new paradigm where speed, transparency, and competitive bidding are automated through advanced technology. (Get Answers For Hard)

The Problem with Traditional Lending

Historically, finding competitive financing was a fragmented and inefficient process. Borrowers and lenders alike spent countless hours making cold calls, submitting redundant documentation, and waiting for manual underwriting reviews. This linear approach created significant bottlenecks. A borrower might secure a quote from one lender only to discover later that a competitor offered significantly better terms. This lack of market visibility often resulted in suboptimal financing structures and delayed closings. (About Lendersa 50 Years)

The traditional model also suffered from information asymmetry. Lenders did not always have immediate access to the full spectrum of available capital, while borrowers struggled to understand the nuances of different loan products. This disconnect led to missed opportunities and increased friction in the transaction lifecycle. The introduction of digital platforms has begun to bridge this gap, but true efficiency requires more than just a website. It requires a systematic approach to capital aggregation. (Loan Types In Los)

AI-Driven Lender Matching

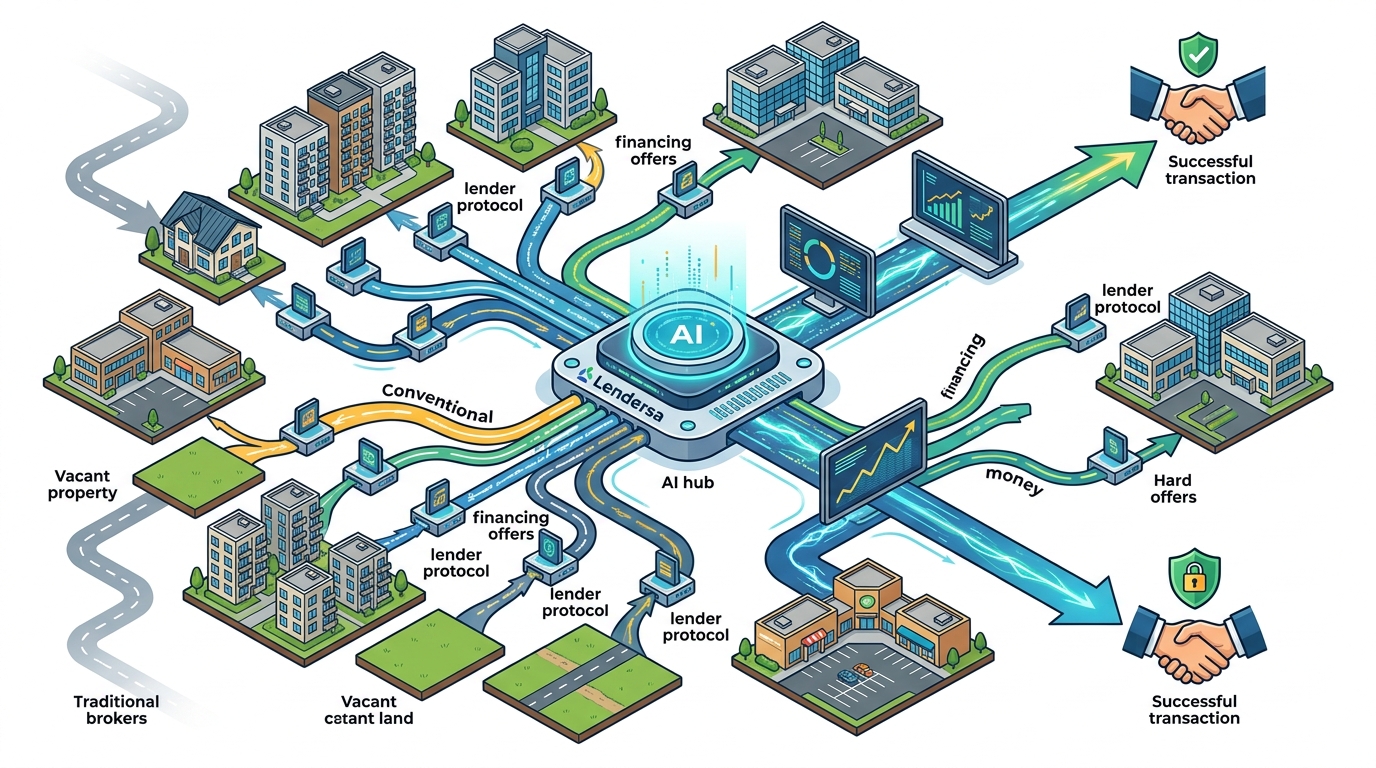

Artificial Intelligence has revolutionized how loan scenarios are evaluated and routed. AI-driven lender matching involves using advanced algorithms to analyze a borrower's profile and instantly identify the most suitable lenders from a vast network. This process eliminates the guesswork associated with manual screening. The system evaluates dozens of lender matrices simultaneously, considering factors such as loan-to-value ratios, credit profiles, property types, and closing timelines. (Compare Hard Money amp)

At the core of this technology is the ability to process complex data points in real time. When a loan scenario is input into an AI system, it does not simply search for a keyword match. It evaluates the entire financial context of the deal. This includes assessing the borrower's equity position, the property's potential after-repair value, and the specific risk appetite of various lenders. The result is a curated list of qualified lenders who are not only willing to lend but are competitively positioned to offer favorable terms.

This technology also addresses the issue of "no Social Security Number" requirements for certain commercial or entity-based loans. By focusing on asset-based metrics rather than just personal credit, AI systems can route deals to private investors and hard money lenders who specialize in equity-based financing. This expands the pool of available capital for borrowers who may not fit traditional bank criteria.

The Multi-Lender Protocol

The Multi-Lender Protocol is a proprietary framework designed to force competition among lenders on behalf of the borrower. Instead of approaching lenders sequentially, this protocol presents the loan request to multiple qualified lenders simultaneously. This creates a competitive environment where lenders are incentivized to offer their best terms to win the business. The protocol operates in distinct phases: search, compare, negotiate, and finalize.

In the search phase, the system identifies hundreds of potential lenders based on the loan scenario. In the compare phase, the AI evaluates the offers from these lenders, balancing speed of closing against cost of capital. The negotiate phase is where the protocol truly shines. By pitting lenders against each other, the system drives down interest rates and fees. This is particularly effective for hard money loans and bridge loans, where speed is critical but cost can vary significantly between providers.

The final phase involves the issuance of a Letter of Intent (LOI). The AI re-runs the search to find lenders who are ready to issue an LOI based on the provided documentation. This ensures that the final selection is not just theoretically competitive but practically executable. The top lender is awarded the loan, while runners-up are kept on standby to mitigate any processing risks. This structured approach minimizes the risk of deal failure due to lender withdrawal or unexpected underwriting hurdles.

Comparing Financing Options

Understanding the differences between various loan types is essential for streamlining the search process. Hard money loans, conventional mortgages, and private capital each serve different purposes and come with distinct risk profiles. Below is a comparison of these primary financing options.

| Loan Type | Primary Use Case | Closing Speed | Typical Lender | Key Advantage |

|---|---|---|---|---|

| Hard Money Loans | Fix and Flip, Bridge Financing | Days | Private Investors | Speed and Equity Focus |

| Conventional Loans | Primary Residence, Investment | 30-45 Days | Banks, Credit Unions | Lower Interest Rates |

| Construction Loans | New Builds, Major Renovations | 2-4 Weeks | Specialized Lenders | Draw-Based Funding |

| Private Capital | Non-QM, Complex Deals | 1-2 Weeks | Private Equity | Flexible Underwriting |

Each of these options requires a different approach to sourcing. Hard money lenders prioritize the asset's value and exit strategy. Conventional lenders focus heavily on borrower credit and income verification. Private capital providers look for unique opportunities that banks might reject. By using a platform that aggregates these diverse sources, borrowers can quickly identify which type of capital aligns with their specific needs.

Key Takeaways

- AI Matching Efficiency: Automated systems can evaluate dozens of lender matrices in seconds, reducing search time from weeks to minutes.

- Competitive Bidding: The Multi-Lender Protocol forces lenders to compete, often resulting in lower interest rates and fees for the borrower.

- Speed to Close: Hard money and bridge loans facilitated through digital platforms can close in days, not months, which is critical for auction purchases.

- Equity Focus: Private lenders and hard money providers prioritize property equity over personal credit scores, opening doors for complex deals.

- LOI Precision: The finalization phase ensures that only lenders ready to issue a Letter of Intent are considered, reducing deal risk.

- Nationwide Reach: Digital platforms connect borrowers with capital across all 50 states, eliminating geographic limitations.

- No SSN Options: Certain commercial and entity-based loans can be sourced without providing a Social Security Number, focusing instead on asset value.

Frequently Asked Questions

How does AI improve the loan search process?

AI improves the loan search process by instantly analyzing a borrower's profile against thousands of lender programs. It identifies the best matches based on risk, cost, and speed, eliminating the need for manual screening and reducing the time to find competitive offers.

What is the Multi-Lender Protocol?

The Multi-Lender Protocol is a method where a loan request is presented to multiple qualified lenders simultaneously. This creates a competitive bidding environment that drives down costs and improves terms for the borrower.

Can I get a loan without a Social Security Number?

Yes, many hard money and private capital lenders focus on the property's equity and value rather than personal credit. These loans are often structured around the asset itself, allowing for financing without a Social Security Number.

How fast can hard money loans close?

Hard money loans can close in as little as a few days. This speed is achieved by focusing on asset-based underwriting and bypassing the lengthy approval processes typical of conventional banks.

What types of properties are eligible for these loans?

Eligible properties typically include residential homes, commercial buildings, vacant land, and properties undergoing start-up construction. The specific criteria depend on the lender's risk appetite and the loan product.

How do I compare loan offers effectively?

Effective comparison involves looking beyond just the interest rate. Factors such as loan-to-value ratios, prepayment penalties, closing costs, and funding timelines must be evaluated. Platforms like Lendersa provide tools to compare these metrics side-by-side.

What is a Letter of Intent (LOI) in lending?

A Letter of Intent (LOI) is a document issued by a lender indicating their willingness to fund a loan under specific terms. It serves as a preliminary agreement before the final underwriting and closing process begins.

Secure Your Competitive Financing Today

Stop searching and let lenders compete for you. By leveraging advanced AI and the Multi-Lender Protocol, you can access the most favorable terms in the market. Whether you need a fast-closing bridge loan or a conventional mortgage, the right capital is just a few clicks away. Start your loan search now and discover how much you could save.