Traditional lending is broken. According to a 2024 analysis by the National Association of Realtors, the average time to close a mortgage has increased by 15% compared to pre-pandemic levels, creating a bottleneck for investors who need speed. This delay is not due to a lack of capital, but rather a failure in the initial matching process. Borrowers are forced to contact dozens of lenders individually, submitting the same sensitive financial data repeatedly. This manual approach is inefficient and often results in missed investment opportunities. The modern solution involves leveraging automated platforms that aggregate capital sources instantly. This guide details the exact steps to initiate a high-efficiency financing comparison using advanced algorithmic routing. (Get Answers For Hard)

Step 1: Define Your Loan Purpose and Property Type

The first step in the financing comparison process is precise categorization. Lenders do not operate in a vacuum; they have specific risk appetites and product lines. You must identify whether your project falls under residential, commercial, or vacant land categories. Furthermore, you must specify the strategy. Are you looking for a fix and flip loan for a short-term renovation? Or do you need a construction loan for ground-up development? The distinction is critical because hard money lenders and conventional banks evaluate these scenarios differently.

Hard money is a short-term loan secured by real estate collateral. It is typically used by investors who need quick access to capital for properties that may not qualify for traditional financing. Conventional loans, by contrast, rely heavily on borrower creditworthiness and income verification. By clearly defining your property type and loan purpose upfront, you allow the comparison engine to filter out irrelevant programs immediately. This prevents the common error of applying for a conventional mortgage when a bridge loan is the appropriate financial instrument.

Step 2: Prepare Your Equity and Asset Documentation

Unlike traditional banking, which focuses on debt-to-income ratios, private capital and hard money lenders focus primarily on the Loan-to-Value (LTV) ratio. This means your equity in the property is your most valuable asset. Before initiating the comparison, you must gather the following documentation:

- Property Appraisal or ARV Estimate: The After Repair Value (ARV) is the projected value of the property after renovations. Lenders use this to determine the maximum loan amount they will provide.

- Renovation Budget: A detailed scope of work and cost estimate. This proves to the lender that you have a realistic plan for increasing the asset's value.

- Proof of Funds: Evidence that you have the cash reserves for the down payment and closing costs. This demonstrates financial commitment and reduces lender risk.

- Property Title Report: A clear title ensures there are no liens or legal encumbrances that would prevent the lender from securing their interest.

Having these documents ready allows the platform to run a preliminary analysis. This step is crucial because it enables the use of proprietary tools like LoanScore™ to evaluate your deal's strength before any formal applications are submitted. This pre-qualification step ensures that you are only matched with lenders who are likely to approve your specific scenario.

Step 3: Utilize the Multi-Lender Protocol

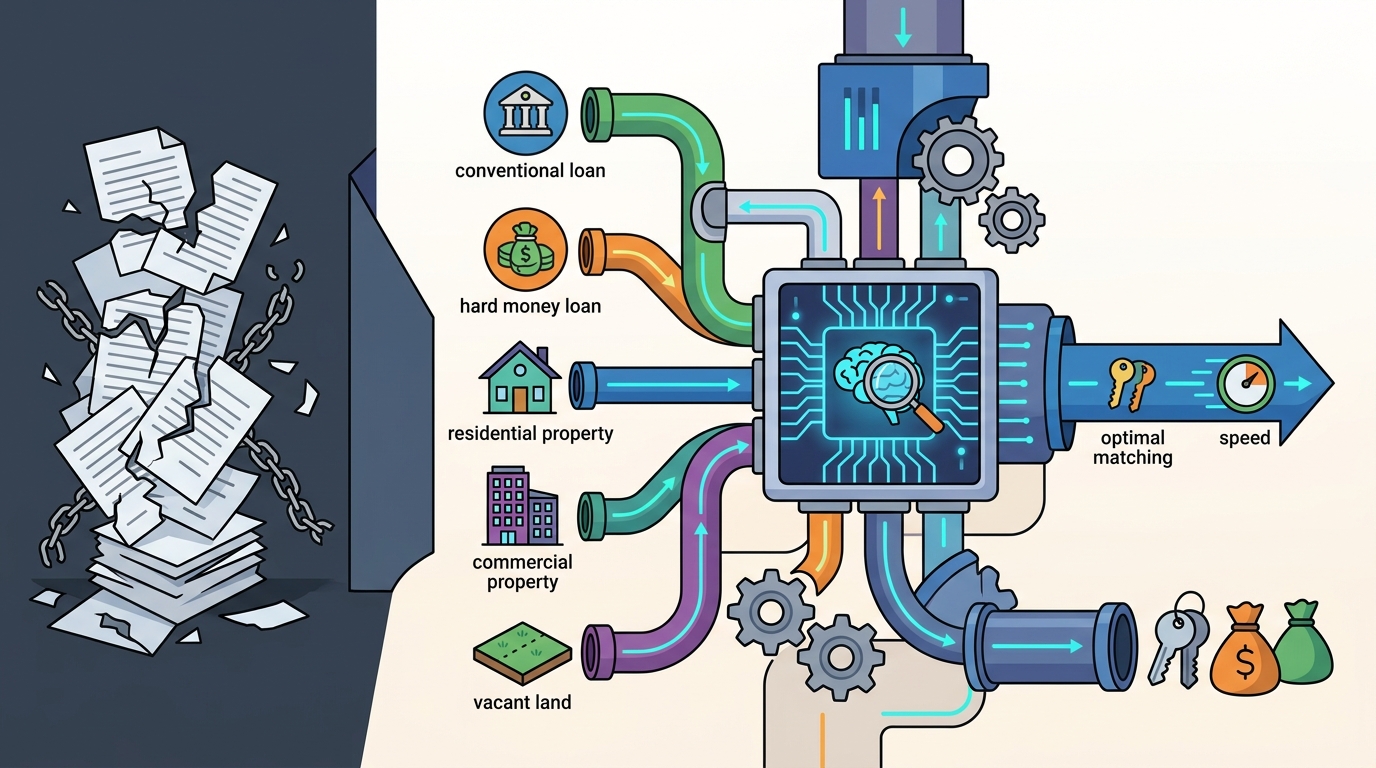

Once your data is prepared, the next step is to engage the Multi-Lender Protocol. This is the core mechanism that differentiates modern comparison platforms from traditional brokerages. Instead of you contacting lenders one by one, you submit your loan scenario to the platform's central engine. The algorithm then routes your request to hundreds of qualified lenders simultaneously.

This protocol operates on a competitive bidding model. By presenting your loan request to multiple qualified lenders at once, the system creates a competitive environment. Lenders are incentivized to offer their best terms to win your business. This process eliminates the need for you to negotiate manually with each institution. The platform handles the initial routing, ensuring that your data is presented in a standardized format that lenders can quickly evaluate. This standardization is vital because it reduces the time lenders spend on underwriting preliminary data, allowing them to focus on pricing.

The Multi-Lender Protocol also supports various loan types, including hard money loans, conventional loans, and small business loans. This versatility allows you to compare disparate capital sources on a level playing field. Whether you are a real estate investor seeking a bridge loan or a business owner looking for working capital, the protocol ensures that you receive offers from the most relevant lenders for your specific needs.

Step 4: Analyze the AI-Generated Matrix

After the protocol routes your request, the platform's AI evaluates the responses. This step involves reviewing a comparative matrix of offers. The AI does not just list the offers; it ranks them based on key metrics such as interest rates, closing speed, loan-to-value ratios, and points. This analysis is critical because the lowest interest rate is not always the best deal. You must consider the total cost of capital, including origination fees and prepayment penalties.

The AI also considers the reliability of the lender. Lenders with a history of fast closings and consistent funding are prioritized. This is particularly important for investors who need to beat the competition at auction. A loan with a slightly higher rate but a guaranteed 5-day closing is often more valuable than a lower-rate loan with a 30-day closing timeline. The platform's LoanCompare™ tool helps visualize these differences, allowing you to make an informed decision based on your specific timeline and budget constraints.

Additionally, the AI checks for compatibility with your credit profile. If you have a less-than-perfect credit history, the platform filters out lenders who have strict credit score requirements. This ensures that you only see offers that you are actually eligible to receive. This filtering process saves time and prevents the frustration of applying for loans that will inevitably be denied. The result is a curated list of viable options that align with your financial reality.

Step 5: Negotiate and Finalize the Best Offer

The final step is to select the best offer and move toward closing. The platform facilitates this by allowing you to negotiate terms directly with the selected lender. Because the lender has already seen your competitive offers, they are more likely to be flexible on points or fees. This negotiation phase is where the value of the comparison process becomes apparent. You have the leverage of multiple competing bids, which forces the top lender to improve their terms to secure your business.

Once you accept an offer, the lender issues a Letter of Intent (LOI). This document outlines the final terms of the loan, including the interest rate, amortization schedule, and closing date. You must review this document carefully to ensure it matches the terms discussed during the negotiation. Any discrepancies should be addressed immediately before signing. After signing the LOI, the lender begins the underwriting process. Because your documentation was prepared in Step 2, this process is typically much faster than traditional lending.

The platform continues to monitor the progress of your loan. If any issues arise, the AI can re-route your request to standby lenders who are ready to step in. This safety net ensures that your deal does not fall through due to unexpected processing delays. The goal is to provide a seamless experience from initial inquiry to funding. By following these steps, you can secure the best possible financing for your project with minimal effort and maximum efficiency.

Comparison of Financing Options

Understanding the differences between various loan types is essential for making the right choice. The table below summarizes the key characteristics of the most common financing options available through the platform.

| Loan Type | Best For | Closing Speed | Primary Focus | Typical LTV |

|---|---|---|---|---|

| Hard Money Loan | Fix and Flip, Bridge Loans | Fast (Days) | Property Equity | 65-75% |

| Conventional Loan | Primary Residence, Investment | Slow (Weeks) | Credit & Income | 80-97% |

| Construction Loan | Ground-Up Development | Medium (Weeks) | Builder Experience | 80-90% |

| Reverse Mortgage | Seniors (62+) | Medium (Weeks) | Home Equity | Up to 100% |

Key Takeaways

- Founder Expertise: Lendersa was founded by Moshon Reuveni, who has been active in the lending industry since 1976, bringing over 50 years of experience to the platform.

- Global Reach: The platform matches borrowers with capital across all 50 states in the USA, Canada, and Puerto Rico.

- Proprietary Tools: The platform utilizes LoanScore™, LoanImprove™, and LendChat™ to help borrowers prepare and pitch their deals effectively.

- Competitive Bidding: The Multi-Lender Protocol pits lenders against each other to drive down rates and improve terms for the borrower.

- No SSN Required: Initial searches and comparisons can be conducted without providing a Social Security Number, protecting borrower privacy.

- Diverse Loan Types: The platform handles Fix and Flip, Construction, Conventional, FHA, USDA, VA, Jumbo, and Commercial loans.

- Speed to Market: Hard money and bridge loans can close in days, not months, which is critical for auction purchases.

Frequently Asked Questions

Do I need a high credit score to use the comparison platform?

No. The platform aggregates lenders who specialize in various credit profiles, including subprime and non-QM loans. The AI filters for lenders who are willing to work with your specific credit situation, focusing more on your equity than your credit score.

How does the Multi-Lender Protocol work?

The protocol routes your loan request to hundreds of lenders simultaneously. These lenders then compete to offer you the best terms. This process eliminates the need for you to contact each lender individually and ensures you receive the most competitive offers available.

Can I compare hard money loans with conventional bank loans?

Yes. The platform allows you to compare hard money lenders, private investors, and big banks side-by-side. This comprehensive view helps you determine which type of capital is best suited for your specific project timeline and financial goals.

What documents do I need to start the process?

You need to provide property details, an appraisal or ARV estimate, a renovation budget, and proof of funds. Having these documents ready allows the platform to run a more accurate match and speeds up the initial underwriting process.

Is my financial information secure?

Yes. The platform uses advanced encryption and security protocols to protect your data. You can view initial offers without providing a Social Security Number, and your sensitive information is only shared with lenders who are serious about funding your deal.

How long does it take to get offers?

Offers can be generated in minutes. The AI instantly matches your scenario with qualified lenders and retrieves their current programs. This speed allows you to make quick decisions, which is essential in competitive real estate markets.

What happens after I accept an offer?

Once you accept an offer, the lender issues a Letter of Intent (LOI). You then review and sign the LOI, after which the lender begins the formal underwriting and closing process. The platform continues to support you through this phase to ensure a smooth closing.

Start Your Financing Comparison Today

Stop wasting time calling lenders one by one. Let the AI do the heavy lifting. Start your financing comparison process now and discover the best rates and terms available for your property. Whether you need a hard money loan, a conventional mortgage, or a commercial loan, the platform is designed to help you secure the capital you need quickly and efficiently.