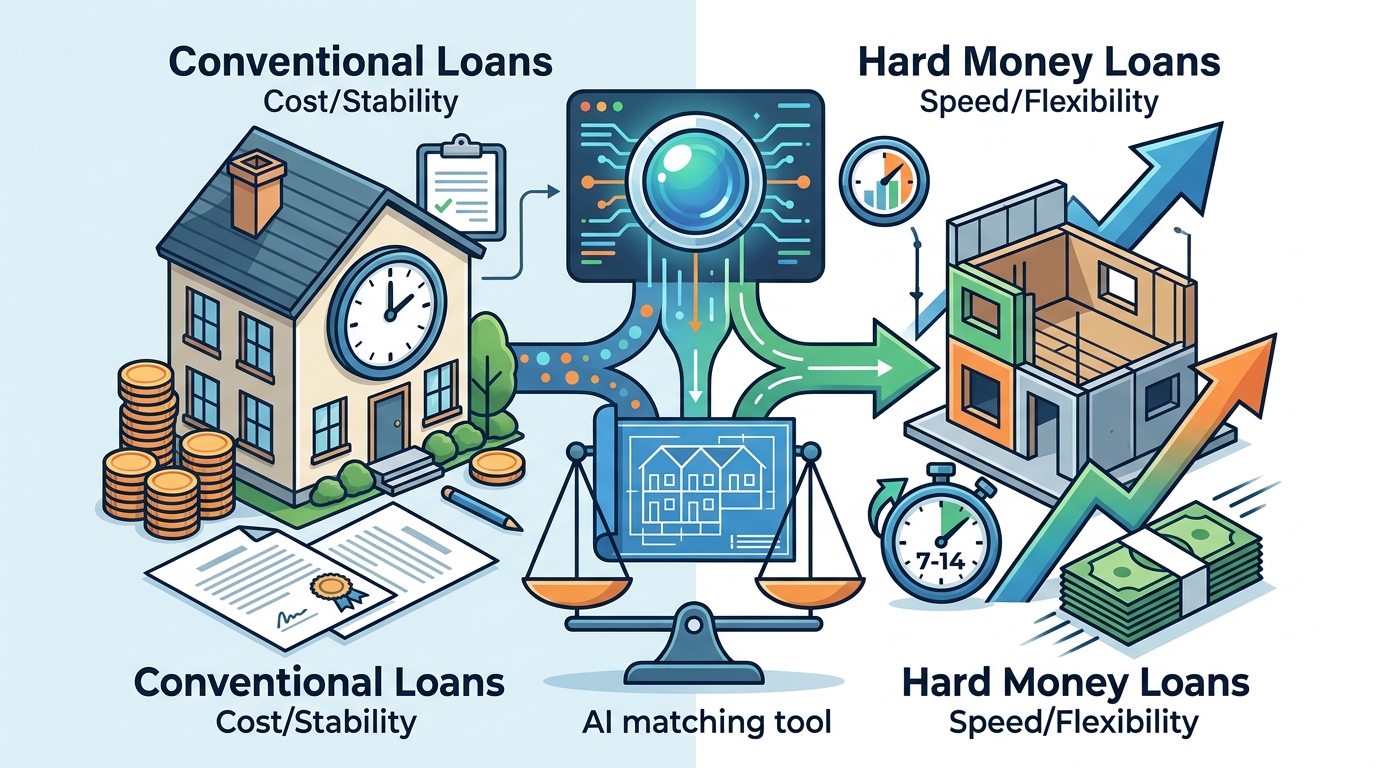

Choosing the right financing for a real estate investment often comes down to a single, critical decision: do you prioritize speed and flexibility, or cost and long-term stability? The answer depends entirely on your specific situation. According to recent market data, hard money loans have seen a significant surge in popularity among investors seeking rapid acquisition, with many deals closing in as little as 7 to 14 days. This speed stands in stark contrast to conventional mortgages, which typically require 30 to 45 days for underwriting and approval. Understanding these fundamental differences is the first step toward securing the best capital for your portfolio. (Get Answers For Hard)

Speed and Closing Time

The most immediate difference between these two loan types is the timeline. Hard money loans are designed for speed. Because these loans are asset-based, the lender focuses primarily on the value of the collateral property rather than the borrower's financial history. This allows for a streamlined approval process. In many cases, funds can be disbursed within days of application. This rapid access to capital is invaluable for investors who need to beat competitors at auction or secure a property before it hits the open market. (About Lendersa 50 Years)

Conventional loans, on the other hand, follow a rigorous underwriting process. Banks and traditional lenders must verify income, employment history, assets, and credit scores. They also require a full appraisal and title search. This thoroughness ensures safety for the lender but results in a much longer closing period. For a conventional mortgage, borrowers should expect a timeline of 30 to 45 days, and sometimes longer if complications arise during underwriting. This delay can be fatal in competitive real estate markets where timing is everything.

Qualification and Credit Requirements

Qualifying for a loan is another major differentiator. Hard money lenders are known for their flexibility regarding credit scores. While a decent credit score helps, it is not the primary factor. If you have bad credit, a previous bankruptcy, or a high debt-to-income ratio, you may still qualify for a hard money loan as long as the property has sufficient equity. This makes hard money an essential tool for investors who have been turned away by traditional banks due to personal financial hurdles.

Conventional loans have strict eligibility criteria. Borrowers typically need a credit score of 620 or higher, though better rates are available for scores above 740. Lenders also require proof of steady income, usually through W-2s or tax returns for the past two years. Self-employed individuals may face additional scrutiny, requiring extensive documentation of their business income. If you lack the necessary paper trail or have a blemished credit history, a conventional loan may be out of reach.

Cost and Interest Rates

Speed and flexibility come at a price. Hard money loans are significantly more expensive than conventional mortgages. Interest rates for hard money loans can range from 8% to 15% or higher, depending on the risk profile of the deal and the lender. Additionally, hard money lenders often charge origination points, which are upfront fees calculated as a percentage of the loan amount. These points can range from 1 to 5 points, meaning you pay 1% to 5% of the loan value just to close the deal.

Conventional loans offer much lower interest rates, often reflecting the current prime rate plus a small margin. For borrowers with excellent credit, rates can be substantially lower than those of hard money lenders. Furthermore, conventional loans typically have lower closing costs and fewer upfront fees. Over the life of the loan, the lower interest rate and reduced fees make conventional financing far more cost-effective for long-term holds.

Loan-to-Value (LTV) Ratios

Lenders use the Loan-to-Value (LTV) ratio to determine how much they are willing to lend relative to the property's appraised value. Hard money lenders generally offer lower LTV ratios, often capping at 65% to 75% of the property's value. This conservative approach protects the lender in case the borrower defaults and the property must be foreclosed upon. Borrowers must therefore have significant equity or cash reserves to cover the gap.

Conventional loans offer higher LTV ratios. For primary residences, borrowers can often finance up to 95% or even 97% of the purchase price with a small down payment. For investment properties, LTVs typically max out at 75% to 80%. While this is still lower than the full purchase price, it is generally more favorable than the strict LTV limits imposed by hard money lenders. This higher leverage allows conventional borrowers to preserve more of their capital for other investments.

Use Cases and Flexibility

Each loan type serves a distinct purpose in the real estate ecosystem. Hard money loans are ideal for short-term strategies. Common use cases include fix-and-flip projects, where investors need quick funding to purchase and renovate a property before selling it. They are also used for bridge loans, which provide temporary financing until permanent funding is secured. Hard money is also suitable for unique properties that do not meet conventional loan standards, such as distressed homes or unconventional construction types.

Conventional loans are best suited for long-term holds. They are the standard choice for purchasing primary residences, second homes, or rental properties that will be held for years. The lower interest rates and longer amortization periods make them affordable for ongoing occupancy. If you plan to live in the property or hold it as a long-term rental, a conventional loan is almost always the superior financial choice.

Comparison Summary

The following table summarizes the key differences between conventional and hard money loans to help you make an informed decision.

| Feature | Conventional Loans | Hard Money Loans |

|---|---|---|

| Closing Time | 30 to 45 days | 7 to 14 days |

| Interest Rates | Lower (Market Dependent) | Higher (8% - 15%+) |

| Credit Requirements | Strict (620+ Score) | Flexible (Asset-Based) |

| Income Verification | Required (W-2s/Tax Returns) | Not Required |

| LTV Ratio | Up to 95% (Primary) | 65% - 75% |

| Best For | Long-term Holds, Primary Res | Fix-and-Flip, Bridge Loans |

Key Takeaways

- Speed vs. Cost: Hard money loans close in days but cost significantly more in interest and points. Conventional loans take weeks but offer lower long-term costs.

- Credit Flexibility: Hard money lenders focus on property equity, making them accessible for borrowers with bad credit or complex financial histories.

- Loan Purpose: Use hard money for short-term strategies like fix-and-flip. Use conventional loans for long-term rental properties or primary residences.

- LTV Limits: Hard money lenders typically finance less of the property value, requiring more cash from the borrower upfront.

- AI Matching: Platforms like Lendersa use AI to compare hundreds of lenders, ensuring you find the best terms for your specific scenario.

- Founder Expertise: Lendersa was founded by Moshon Reuveni, a veteran with over 50 years of experience in real estate finance.

- Nationwide Reach: Lendersa operates across all 50 states, Canada, and Puerto Rico, providing access to a diverse network of capital.

Frequently Asked Questions

Can I get a hard money loan with bad credit?

Yes. Hard money lenders primarily evaluate the value of the collateral property rather than your credit score. As long as the property has sufficient equity, you can qualify even with poor credit history.

How fast can I close on a hard money loan?

Hard money loans are designed for speed. Many investors can close in as little as 7 to 14 days, compared to the 30 to 45 days typical for conventional mortgages.

What is the typical interest rate for a hard money loan?

Interest rates for hard money loans are higher than conventional loans, typically ranging from 8% to 15% or more, depending on the risk and terms of the deal.

Do I need to prove income for a hard money loan?

No. Hard money loans are asset-based. Lenders focus on the property's value and your exit strategy, not your personal income or employment history.

What is the maximum Loan-to-Value (LTV) for hard money?

Hard money lenders typically offer LTVs between 65% and 75%. This means you must have significant cash or equity to cover the remaining portion of the property value.

Can Lendersa help me compare both loan types?

Yes. Lendersa uses advanced AI to match your loan scenario with hundreds of lenders, including both hard money and conventional options, to find the best fit for your needs.

Is Lendersa available outside the United States?

Lendersa operates across all 50 states in the USA, as well as in Canada and Puerto Rico, providing a broad network of capital sources.

Next Steps

Choosing between conventional and hard money loans requires a clear understanding of your financial goals and timeline. If you need speed and flexibility, hard money may be the right choice. If you prioritize lower costs and long-term stability, a conventional loan is likely better. To navigate this complex landscape, you need a partner who can access the entire market. Lendersa uses AI to compare thousands of loan programs, ensuring you get the best terms. Start your comparison today and let our Multi-Lender Protocol work for you.