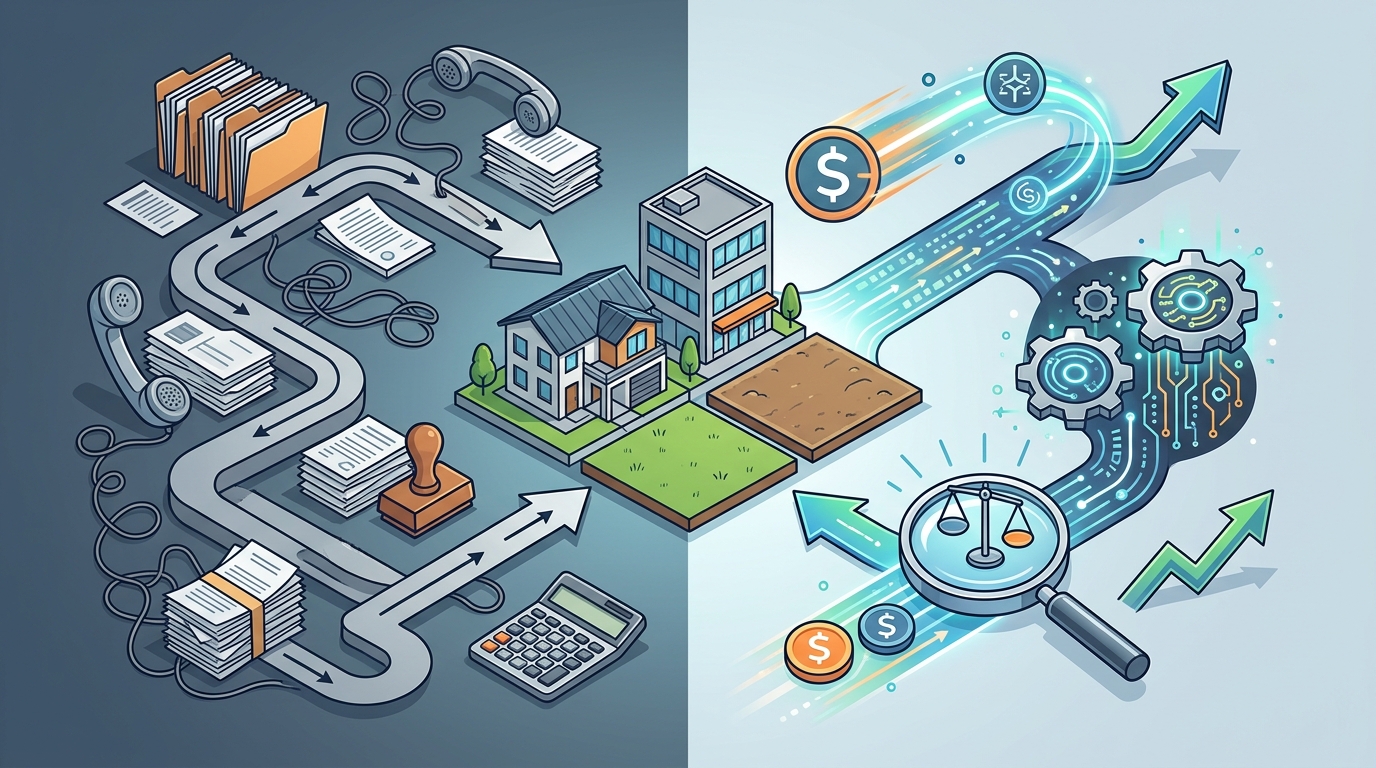

Securing capital for a real estate acquisition has fundamentally shifted from a manual phone call to a data-driven algorithmic process. According to recent industry analyses, borrowers who utilize automated comparison platforms secure loans up to 30% faster than those relying on single-lender inquiries. This efficiency gap exists because traditional methods force you to hunt for capital, whereas modern technology allows capital to hunt for you. Understanding this dynamic is the first step toward unlocking the most favorable terms for your specific property type. (Get Answers For Hard)

Understanding Financing Types

Before engaging with any capital source, you must define the nature of your investment. The real estate market offers a diverse array of loan products, each designed for specific scenarios. Hard money loans are short-term, asset-based loans typically used by investors for fix-and-flip projects or bridge financing. These loans prioritize speed and equity over credit scores, allowing for rapid closings in days rather than months. Hard money lenders operate outside traditional banking regulations, providing flexibility for complex deals. (About Lendersa 50 Years)

Conventional loans, on the other hand, are backed by government-sponsored enterprises like Fannie Mae or Freddie Mac. These are ideal for primary residences or long-term hold properties where the borrower has strong credit and documented income. FHA loans offer lower down payment requirements for qualified buyers, while VA loans provide zero-down options for eligible veterans. Understanding the distinction between these products is critical because applying for the wrong type can delay your closing or result in immediate denial. (Loan Types In Los)

For commercial properties, the landscape shifts again. Commercial loans often require larger down payments and have shorter amortization periods. They are evaluated based on the property's income-generating potential rather than just the borrower's personal financials. Commercial lending also includes SBA loans, which offer government-backed guarantees to small business owners purchasing real estate for their operations. Each category requires a distinct approach to presentation and negotiation.

The Multi-Lender Protocol Advantage

The traditional model of real estate financing is broken. Borrowers typically contact one lender, wait for a quote, and then move to the next, creating a linear and inefficient process. This method is slow, stressful, and often results in suboptimal terms because you lack competitive leverage. The Multi-Lender Protocol changes this dynamic by introducing competition into the lending process.

When you submit your loan scenario through a platform like Lendersa, your request is not sent to a single bank. Instead, it is distributed to a network of hundreds of lenders, including big banks, credit unions, private investors, and hard money brokers. These lenders compete for your business by offering their best terms. This competition drives down interest rates and increases loan amounts, ensuring you receive the most favorable deal available in the market.

This protocol also includes a negotiation phase. The AI system evaluates the initial offers and pits the lenders against each other to secure better terms. This automated negotiation happens in real-time, saving you hours of phone calls and emails. The result is a streamlined process where you sit back and let the market work for you. Learn more about the Multi-Lender Protocol to understand how this technology disrupts traditional lending.

AI vs. Traditional Brokers

Many borrowers wonder if an AI-driven platform can replace a traditional mortgage broker. The answer is not that one replaces the other, but that AI augments the broker's capabilities with unprecedented scale. Traditional brokers rely on their personal relationships with a limited number of lenders. While this can be effective, it inherently limits the borrower to only those specific relationships.

AI platforms aggregate data from thousands of lenders, including those a human broker might not know or have access to. This broader net captures niche programs, such as 100% LTV loans or specific state-based fix-and-flip programs. Furthermore, AI eliminates human bias and error. The algorithm evaluates your loan scenario against strict criteria without emotional fatigue or subjective judgment. Explore Lendersa's proprietary AI tools to see how technology enhances accuracy.

However, the human element remains valuable for complex negotiations. The best approach combines AI's speed and breadth with strategic human oversight. Platforms like Lendersa facilitate this by providing a dashboard where you can review offers and make informed decisions. The AI handles the heavy lifting of data aggregation, while you retain control over the final selection. This hybrid model offers the efficiency of technology with the nuance of human expertise.

Pre-Qualification Tools

Before you even submit a loan application, you can optimize your profile using specialized pre-qualification tools. These tools analyze your financial situation and provide actionable insights to improve your loan eligibility. One such tool is the Loan Score™, which evaluates your creditworthiness and property value to predict your likelihood of approval.

Another critical tool is LoanImprove™, which offers personalized recommendations to enhance your loan profile. This might include suggestions for debt consolidation, credit score improvement, or property documentation. By addressing these issues upfront, you position yourself as a lower-risk borrower, which can lead to better terms. Access pre-application options to start improving your standing.

These tools also help you understand the "pitch" of your loan. Just as you would pitch a business idea to an investor, you must present your real estate deal in a way that highlights its strengths. Lendersa's LendChat™ feature allows you to refine your loan narrative, ensuring that all relevant details are communicated clearly to potential lenders. This preparation is essential for securing funding, especially for non-standard properties or complex financial situations.

Financing Options Comparison

To help you navigate the various options, here is a comparison of common financing types available through the Lendersa network.

| Loan Type | Best For | Speed | Credit Requirement | Typical LTV |

|---|---|---|---|---|

| Hard Money | Fix & Flip, Bridge | Fast (Days) | Flexible | Up to 100% |

| Conventional | Primary Residence | Medium (Weeks) | Good to Excellent | Up to 97% |

| FHA Loans | First-Time Buyers | Medium (Weeks) | Fair to Good | Up to 96.5% |

| Commercial | Investment Properties | Variable | Strong Business Plan | Up to 80% |

| SBA Loans | Small Business Real Estate | Slow (Months) | Good | Up to 90% |

Key Takeaways

- Competition Lowers Costs: Using a multi-lender protocol can reduce interest rates by forcing lenders to bid for your business.

- Speed Matters: Hard money loans can close in days, crucial for competitive markets or auction purchases.

- AI Enhances Accuracy: Proprietary tools like Loan Score™ provide precise eligibility assessments beyond simple credit checks.

- Founder Expertise: Lendersa was founded by Moshon Reuveni, a veteran with over 50 years of industry experience since 1976.

- Nationwide Coverage: The platform operates across all 50 states, Canada, and Puerto Rico, ensuring local program access.

- No SSN Required Initially: You can view offers instantly without providing your Social Security Number, protecting your privacy.

- Comprehensive Network: Access includes big banks, credit unions, private investors, and hard money brokers in one dashboard.

Frequently Asked Questions

How does Lendersa find the best loan for me?

Lendersa uses advanced AI to search thousands of lender programs simultaneously. It matches your specific property type and loan purpose with the most suitable offers, then negotiates the best terms on your behalf.

Do I need a good credit score to get a hard money loan?

Not necessarily. Hard money lenders focus primarily on the equity in the property rather than your credit score. This makes it an excellent option for borrowers with bad credit or no income documentation.

Can I compare hard money and conventional loans side by side?

Yes. The Lendersa platform allows you to view and compare offers from both hard money lenders and conventional banks in a single dashboard, helping you choose the best fit for your financial goals.

Is Lendersa a direct lender?

No, Lendersa is a technology platform that connects borrowers with a network of lenders. It acts as a bridge between you and hundreds of capital sources, including banks, private investors, and brokers.

How long does it take to get a loan offer?

You can view hard money offers or bank loans instantly after submitting your initial scenario. The AI evaluates your data in real-time to provide immediate preliminary offers.

What is the LoanScore™ tool?

LoanScore™ is a proprietary tool that analyzes your financial profile and property details to predict your loan eligibility and suggest improvements before you apply.

Does Lendersa operate internationally?

Lendersa primarily serves borrowers in the USA, Canada, and Puerto Rico, leveraging a vast network of domestic and regional lenders.

Start Your Financing Journey

Stop searching and let lenders compete for you. Whether you are looking for a fix-and-flip loan, a conventional mortgage, or commercial financing, the right capital is waiting. Visit the Borrowers Portal to submit your loan scenario and view offers instantly. Experience the power of AI-driven lending and secure the best deal for your property purchase today.