Real estate financing has evolved from a manual, relationship-driven process into a data-driven ecosystem where speed and precision dictate success. According to recent industry analyses, the average time to close a conventional mortgage has increased by 15% over the last three years due to stricter regulatory underwriting standards. In contrast, hard money lenders can often fund deals in as little as 7 to 14 days. This disparity creates a critical decision point for investors and homeowners alike. Understanding the mechanical differences between these two capital sources is no longer optional; it is a fundamental requirement for financial agility in the current market. (Get Answers For Hard)

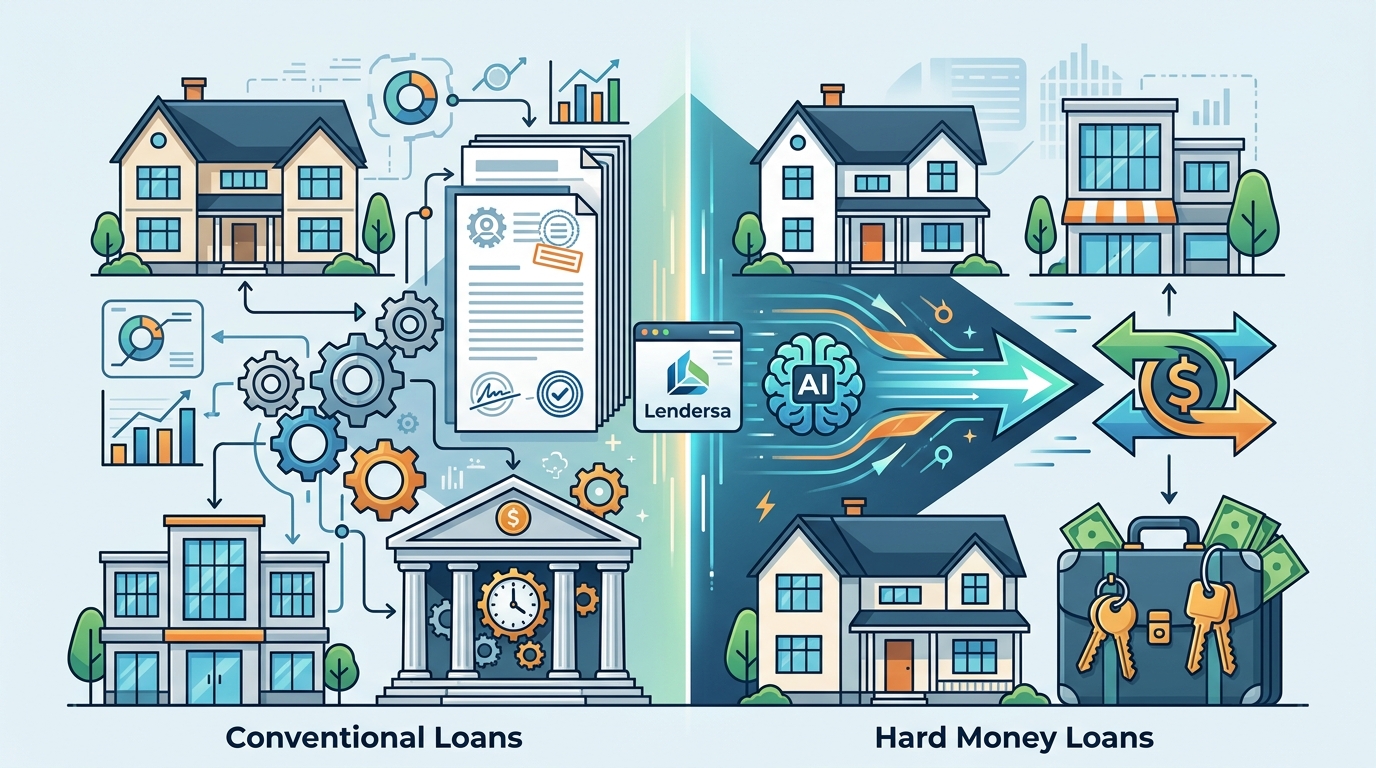

What is Hard Money?

Hard money is a short-term, asset-based loan provided by private investors or companies. The defining characteristic of this financing vehicle is that the lender focuses primarily on the collateral value of the property rather than the borrower's personal financial history. This makes it an essential tool for real estate investors who need capital quickly to acquire, renovate, or bridge a gap in funding. (About Lendersa 50 Years)

Unlike traditional banking, hard money lenders operate with a different risk model. They are willing to fund properties that are in poor condition or have complex ownership structures. This flexibility comes at a price, but for those who understand the mechanics, it offers unparalleled access to liquidity. The process is streamlined because the evaluation criteria are binary: does the property have enough equity to secure the loan? (Loan Types In Los)

For investors engaging in fix-and-flip projects, hard money provides the necessary speed to beat competitive bidding situations. The ability to close in days rather than months can mean the difference between securing a profitable deal and losing it to another buyer. Furthermore, these loans are often interest-only, which preserves cash flow during the renovation phase. (Compare Hard Money amp)

What is Conventional Financing?

Conventional financing refers to loans that are not insured or guaranteed by a government agency like the FHA, VA, or USDA. These loans are typically offered by banks and credit unions and are subject to strict underwriting guidelines established by Fannie Mae and Freddie Mac. The primary focus of conventional lending is the borrower's creditworthiness, debt-to-income ratio, and stable income history. (Compare Hard Money amp)

This type of financing is ideal for primary homeowners or long-term investors who plan to hold the property for an extended period. Conventional loans offer significantly lower interest rates compared to private capital sources. They also provide longer amortization periods, typically 15 to 30 years, which results in lower monthly payments and greater financial stability.

However, the approval process is rigorous. Borrowers must provide extensive documentation, including tax returns, W-2s, and bank statements. Any discrepancies in this paperwork can lead to delays or denial. Additionally, conventional loans often require a minimum down payment of 3% to 20%, depending on the loan type and borrower profile. The emphasis is on financial hygiene and long-term repayment capacity.

Key Differences in Underwriting

The fundamental divergence between hard money and conventional loans lies in the underwriting philosophy. Hard money lenders evaluate the