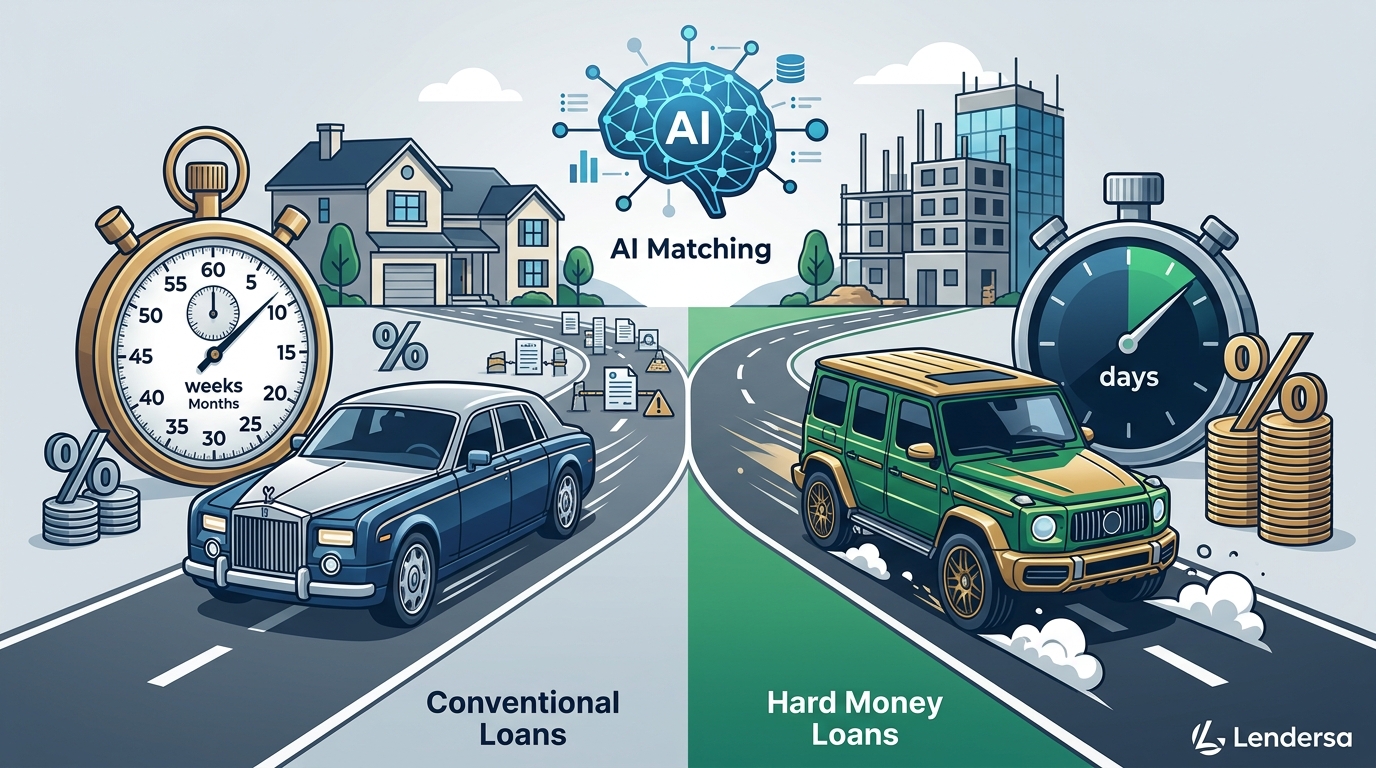

Choosing the right financing vehicle is the single most critical decision in any real estate transaction. The difference between conventional and hard money loans often dictates whether a deal closes in thirty days or thirty minutes. According to recent industry data, hard money lenders typically offer closing times measured in days rather than months, providing a speed advantage that conventional banks simply cannot match. This speed comes at a cost, however, as hard money interest rates are significantly higher than traditional mortgage rates. Understanding these trade-offs is essential for investors and homeowners alike. (Get Answers For Hard)

Speed and Closing Timeline

The most immediate difference between these two loan types is the timeline. Hard money loans are designed for speed. Lendersa® utilizes a Multi-Lender Protocol to match borrowers with capital instantly, allowing for closings in as little as a few days. This is crucial for investors who need to beat competitors at auction or secure a property before it hits the open market. (About Lendersa 50 Years)

In contrast, conventional loans involve a rigorous underwriting process. Banks require extensive documentation, appraisals, and credit checks. This process can take 30 to 60 days or longer. While conventional loans offer stability, they lack the agility required for time-sensitive real estate opportunities. For those needing to close quickly, hard money bridge loans are the superior choice. (Compare Hard Money amp)

Eligibility and Credit Requirements

Conventional loans are heavily dependent on the borrower's financial history. Lenders look at credit scores, debt-to-income ratios, and verified income documentation. If you have bad credit or no income docs, securing a conventional loan can be nearly impossible. Hard money loans, however, focus on the asset. The value of the property you are purchasing or refinancing is the primary collateral. This makes hard money accessible to borrowers who have been denied by traditional banks due to credit issues or complex income situations.

Hard money lenders are private investors or companies that lend their own capital. They are less concerned with your past financial mistakes and more focused on the future value of the property. This equity-based approach allows for greater flexibility in loan structuring. You can view hard money offers or bank loans instantly without needing to provide a Social Security Number for initial matching.

Cost and Interest Rates

Speed and flexibility come with a premium. Hard money loans typically carry higher interest rates than conventional mortgages. This is because the lender is taking on more risk by lending based on asset value rather than borrower creditworthiness. The cost is often justified by the speed of funding and the ability to close deals that would otherwise be lost.

Conventional loans offer lower interest rates and longer terms, making them more affordable over the life of the loan. However, the higher cost of hard money is often a strategic investment for real estate investors who plan to refinance into a conventional loan once the property is stabilized. Lendersa® helps borrowers compare these costs across hundreds of lenders to find the most competitive rates available.

Loan-to-Value (LTV) Ratios

Loan-to-Value (LTV) ratios differ significantly between the two loan types. Conventional loans often allow for LTVs up to 97% for primary residences, meaning borrowers can put down as little as 3% to 5%. Hard money lenders typically offer lower LTVs, often around 65% to 75% of the property's after-repair value (ARV). This requires investors to have more cash on hand for down payments.

Understanding LTV is critical for determining how much capital you need to bring to the table. Hard money lenders may also offer 100% LTV options in specific cases, but these are rare and come with stricter terms. Lendersa® provides tools like LoanScore™ to help borrowers understand their eligibility and potential LTV ratios before applying.

AI-Driven Loan Matching

Traditionally, finding the right lender involved calling dozens of banks and private investors. This process was time-consuming and often yielded inconsistent results. Lendersa® revolutionizes this by using advanced AI to instantly match your loan scenario with hundreds of hard money lenders, private money lenders, and banks. The AI evaluates the best hard money lenders and bridge loans for you, balancing speed and cost to find the absolute best program for your specific property type.

The platform pits lenders against each other to negotiate the best terms. By presenting your loan request to multiple qualified lenders simultaneously, we create a competitive environment that drives them to offer their best terms to win your business. This Multi-Lender Protocol ensures you get the most favorable deal without the hassle of individual negotiations.

| Feature | Conventional Loans | Hard Money Loans |

|---|---|---|

| Closing Time | 30-60+ Days | Days to Weeks |

| Credit Score Requirement | High (620+) | Flexible/Asset-Based |

| Interest Rates | Lower | Higher |

| Primary Focus | Borrower Creditworthiness | Property Value (LTV) |

| Best For | Primary Residences, Long-Term Holds | Fix and Flip, Auctions, Bridge Loans |

Key Takeaways

- Speed vs. Cost: Hard money loans close in days but cost more in interest. Conventional loans are cheaper but slower.

- Eligibility: Hard money focuses on property equity, making it ideal for those with bad credit or no income docs.

- LTV Ratios: Conventional loans offer higher LTVs for primary homes, while hard money focuses on ARV for investment properties.

- AI Matching: Lendersa® uses AI to compare hundreds of lenders, ensuring you get the best terms without manual searching.

- Multi-Lender Protocol: Our system pits lenders against each other to negotiate the best deal for your specific scenario.

- Tool Integration: Utilize LoanScore™ and LoanImprove™ to prepare your deal for faster approval.

- Nationwide Coverage: Lendersa® matches borrowers with capital across all 50 states, Canada, and Puerto Rico.

Frequently Asked Questions

What is the main difference between conventional and hard money loans?

The main difference is the underwriting focus. Conventional loans rely on borrower credit and income, while hard money loans rely on the value of the collateral property.

Can I get a hard money loan with bad credit?

Yes, hard money lenders primarily look at the equity in the property. Bad credit or lack of income documentation is often acceptable if the property has sufficient value.

How fast can I close with a hard money loan?

Hard money loans can close in days, not months. This speed is achieved by bypassing the lengthy underwriting processes required by traditional banks.

What is the Multi-Lender Protocol?

The Multi-Lender Protocol is a Lendersa® technology that presents your loan request to multiple qualified lenders simultaneously to negotiate the best terms.

Do I need to provide a Social Security Number to start?

For initial matching and viewing offers, Lendersa® allows you to view hard money offers or bank loans instantly without needing to provide a Social Security Number.

What types of properties are eligible for hard money loans?

Hard money loans are available for residential, commercial, vacant land, and start-up construction properties, including fix and flip projects.

How does Lendersa® help me find the best loan?

Lendersa® uses advanced AI to search thousands of lender programs, compare them, and negotiate on your behalf to find the lowest rates and fastest closings.

Find Your Best Loan Today

Stop searching and let lenders compete for you. Whether you need a fast closing for a fix and flip or a conventional mortgage for your primary home, Lendersa® connects you with the right capital. Start your loan application now and discover how our AI can save you time and money. Visit our FAQ for more details on our process.